ODDLPRICE Function

The ODDLPRICE function is one of the financial functions. It is used to calculate the price per $100 par value for a security that pays periodic interest but has an odd last period (it is shorter or longer than other periods).

Syntax

ODDLPRICE(settlement, maturity, last_interest, rate, yld, redemption, frequency, [basis])

The ODDLPRICE function has the following arguments:

| Argument | Description |

|---|---|

| settlement | The date when the security is purchased. |

| maturity | The date when the security expires. |

| last_interest | The last coupon date. This date must be before the settlement date. |

| rate | The security interest rate. |

| yld | The annual yield of the security. |

| redemption | The redemption value of the security, per $100 par value. |

| frequency | The number of interest payments per year. The possible values are: 1 for annual payments, 2 for semiannual payments, 4 for quarterly payments. |

| basis | The day count basis to use, a numeric value greater than or equal to 0, but less than or equal to 4. It is an optional argument. The possible values are listed in the table below. |

The basis argument can be one of the following:

| Numeric value | Count basis |

|---|---|

| 0 | US (NASD) 30/360 |

| 1 | Actual/actual |

| 2 | Actual/360 |

| 3 | Actual/365 |

| 4 | European 30/360 |

Notes

Dates must be entered by using the DATE function.

How to apply the ODDLPRICE function.

Examples

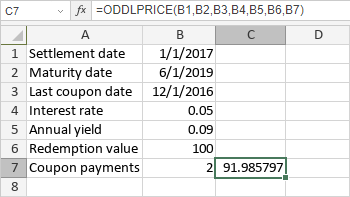

The figure below displays the result returned by the ODDLPRICE function.