Your AI-Powered Senior Quant Researcher.

Discover alpha. Evaluate factors. Monitor decay. Backtest strategies.

All through natural language — in any AI coding assistant.

Quick Start · What Can It Do · Multi-Market · Skills · Contribute

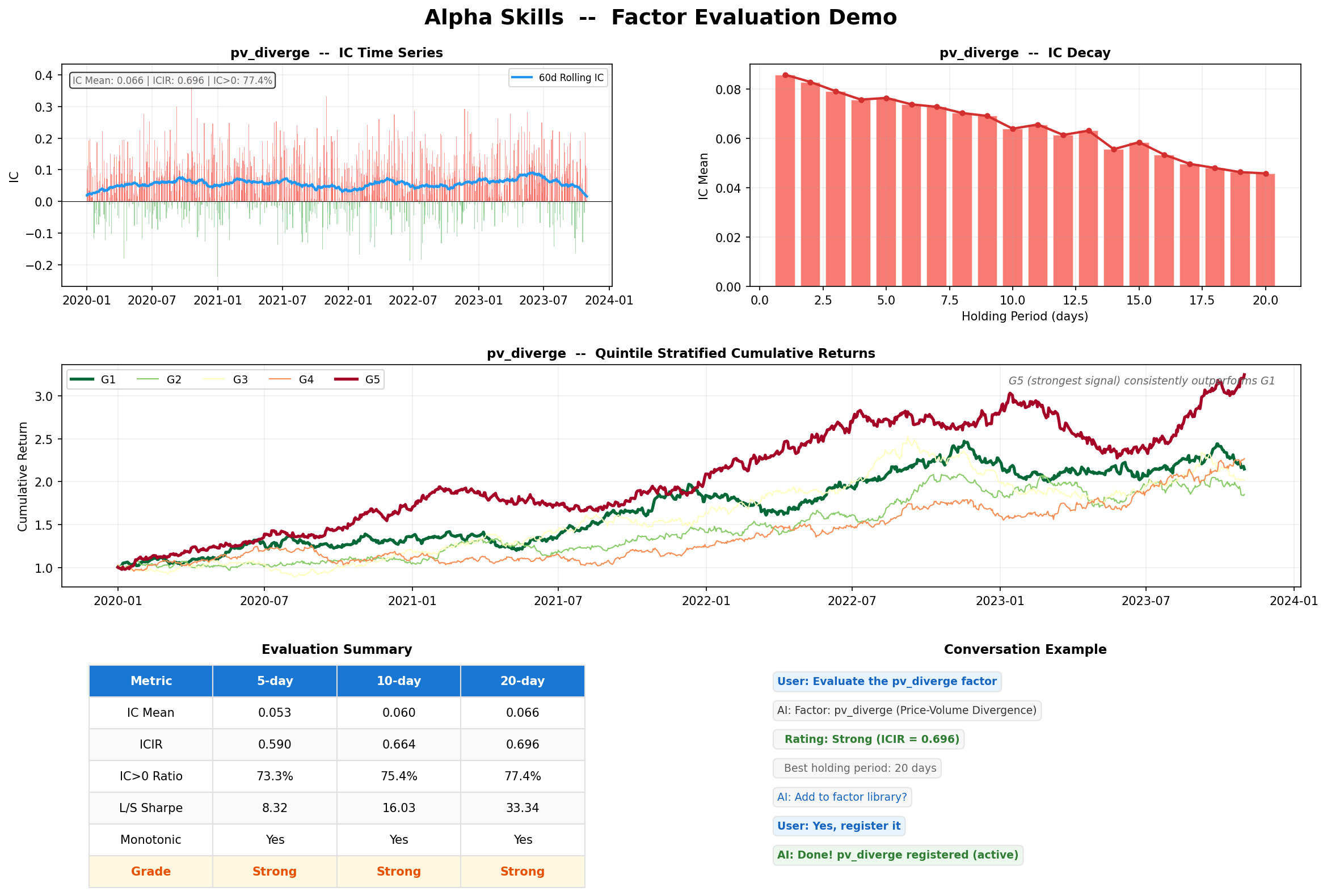

--- > **Hiring a quant researcher costs $300K/year. This one is free, open-source, and works 24/7.** > > Alpha Skills turns any AI coding assistant into a senior quantitative researcher. It discovers factors, evaluates them with institutional-grade methodology (IC/ICIR/quintile/robustness), monitors for alpha decay, and runs multi-factor backtests — all from a single sentence. > > **招一个量化研究员年薪百万。这个免费、开源、7×24小时工作。**  --- ## What Can It Do **You say one sentence. It does the rest.** ``` You: "Evaluate the price-volume divergence factor" AI: 📊 IC Mean=0.066 | ICIR=0.696 | Rating: ⭐ Strong Quintile spread monotonic. Best holding period: 20 days. Report saved → output/eval_pv_diverge.png You: "Mine 50 candidate factors and show me the best ones" AI: ⛏️ Scanned 50 candidates → 12 passed IC screen Top: PV divergence 20d (ICIR=0.70), Low downside vol (ICIR=0.53)... Register to library? You: "Backtest using my top 3 factors" AI: 📈 Sharpe=0.74 | MaxDD=-13.9% | Profit Factor=2.24 Gate check: ✓ PF>1 ✓ MDD>-25% ✗ Sharpe<1.0 ``` No boilerplate. No notebooks. No 200 lines of pandas. Just results. ## Skills Reference | Skill | What It Does | Try Saying | |-------|-------------|------------| | 🔍 **alpha-discover** | Design factors from natural language | "find me a low-volatility factor" | | 📊 **alpha-evaluate** | IC / ICIR / quintile / long-short / robustness | "evaluate reversal_5" | | ⛏️ **alpha-mine** | Auto-mine factor candidates, IC screen, rank | "mine 50 factors" | | 📚 **alpha-library** | Register, list, search, retire factors (SQLite) | "show my factor library" | | 📈 **alpha-backtest** | Single & multi-factor portfolio backtest | "backtest with pv_diverge + turnover" | | 🏥 **alpha-monitor** | Detect IC decay, crowding, regime shift | "check factor health" | | 📋 **alpha-report** | Panoramic, deep-dive, comparison reports | "generate factor report" | | 📡 **alpha-signal** | Daily trading signal — target portfolio output | "today's signals" / "生成信号" | | 🤖 **alpha-autopilot** | Autonomous loop: mine → evaluate → register → monitor → retire | "run autopilot" / "自动驾驶" | ## Quick Start ### 1. Get the skills ```bash git clone https://github.com/VernonOY/alpha-skills.git ``` ### 2. Load into your AI assistant | Platform | How | |----------|-----| | **Cursor** | Copy `skills/alpha-*/SKILL.md` → `.cursorrules` | | **Windsurf** | Copy → `.windsurfrules` | | **Claude Code** | `cp -r skills/alpha-* ~/.claude/skills/` | | **Any LLM** | Paste SKILL.md as system prompt | ### 3. Install Python deps ```bash pip install pandas numpy scipy matplotlib pyarrow pip install tushare # A-share pip install yfinance # US / HK ``` ### 4. Talk to it ``` "evaluate the momentum_20 factor" "mine volatility factors" "backtest my top 3 factors, 2022 to 2025" ``` ## Multi-Market: A-Share · Hong Kong · US Works out of the box for three markets. Auto-adapts trading rules per market: | | A-share 🇨🇳 | Hong Kong 🇭🇰 | US 🇺🇸 | |---|---|---|---| | **Data** | Tushare Pro | Yahoo Finance | Yahoo Finance | | **Price Limit** | ±10% | None | None | | **T+N** | T+1 | T+0 | T+0 | | **Cost** | 0.3% | 0.2% | 0.1% | | **Benchmark** | CSI 300 | HSI | S&P 500 | | **Pool** | 5000+ stocks | 78 HSI constituents | 143 S&P 500 | Switch markets in one line: ```markdown MARKET: US DATA_MODULE: examples.us_data_yfinance ``` **Bring your own data.** Write a 7-function Python adapter for Bloomberg, AkShare, Binance, or any source — [see interface spec](examples/README.md). ## How It Works ``` ┌─────────────────────────────────────────────┐ │ You (natural language) │ ├─────────────────────────────────────────────┤ │ AI Coding Assistant │ │ (Cursor / Windsurf / Claude Code / ...) │ ├─────────────────────────────────────────────┤ │ Alpha Skills (7 SKILL.md) │ │ discover · evaluate · mine · library │ │ backtest · monitor · report │ ├─────────────────────────────────────────────┤ │ Python (pandas/numpy/scipy/matplotlib) │ │ → factor computation │ │ → IC/ICIR/quintile evaluation │ │ → portfolio backtesting │ │ → SQLite factor registry │ ├─────────────────────────────────────────────┤ │ Data: Tushare │ YFinance │ CSV │ Custom │ └─────────────────────────────────────────────┘ ``` **Zero framework dependency.** Each skill is a self-contained Markdown file. The AI reads it, writes the Python, runs it. Nothing to install except standard data science packages. ## Evaluation Pipeline Your AI quant researcher doesn't just compute IC. It runs a **4-level institutional-grade evaluation**: | Level | What | Speed | |-------|------|-------| | **L0** | Syntax + data validation | instant | | **L1** | Quick IC screen (sampled 200 stocks × 2 years) | <30s | | **L2** | Full: IC series, ICIR, quintile returns, long-short, monotonicity | 1-3 min | | **L3** | Robustness: parameter perturbation, rolling window, start-date sensitivity | 5-15 min | Plus optional **[qtype](https://github.com/VernonOY/qtype)** pre-flight — static analysis to catch look-ahead bias before you waste compute on fake alpha. ## Factor Mining Engine `alpha-mine` systematically searches the factor expression space: **3 mining strategies:** - **Template-based** — momentum, mean-reversion, volatility, volume, composite templates × multiple window sizes - **Combinatorial** — chain operators: `cs_rank(ts_corr(close, volume, 20))` - **Mutation** — take a known strong factor, mutate parameters/operators **Pipeline:** Generate 50+ candidates → IC quick screen → full evaluate top 10 → LLM judges economic intuition → present ranked results **Overfitting guard:** Every surviving factor gets an **economic intuition score** (Strong / Moderate / Weak). Factors without a clear behavioral story are flagged as potential data mining. ## Built-in Factors (25+) | Category | Factors | |----------|---------| | **Price-Volume** | momentum · reversal · volatility · pv_diverge · rsi · macd · bollinger · atr_ratio · turnover · abnormal_turnover | | **Fundamental** | roe · roa · gross_margin · net_profit_growth · revenue_growth | | **Valuation** | pe_ttm · pb · ps_ttm · dividend_yield · peg | | **Composite** | quality_score · value_score · growth_momentum | All gate checks and evaluation thresholds are **user-configurable**: ```markdown GATE_SHARPE: 1.0 GATE_MAX_DRAWDOWN: -0.25 GATE_PROFIT_FACTOR: 1.0 EVAL_ICIR_STRONG: 0.5 ``` ## What's New **v0.3 — Autopilot & Live Signals** - `alpha-signal`: daily trading signal generator — outputs target portfolio from active factors - `alpha-autopilot`: autonomous research loop — auto-mine, evaluate, register, monitor, retire - Professional knowledge base: 6 expert-level reference documents (2,795 lines) **v0.2 — Automated Factor Mining** - `alpha-mine`: systematically search factor expression space, IC screen, economic intuition scoring - All skills fully self-contained — zero external package dependencies - Optional [qtype](https://github.com/VernonOY/qtype) pre-flight check **v0.1 — Initial Release** - 7 core skills · A-share/HK/US support · bilingual EN/ZH · multi-platform ## Roadmap - [x] 9 skills (discover / evaluate / mine / library / backtest / monitor / report / signal / autopilot) - [x] Daily signal generation (target portfolio output) - [x] Autonomous research loop (mine → evaluate → register → monitor → retire) - [x] Professional knowledge base (6 expert-level documents, 2,795 lines) - [x] A-share, HK, and US market support - [x] Market-aware trading rules - [x] Automated factor mining (template + combinatorial + mutation) - [x] Custom data source support - [x] Multi-platform (Cursor, Windsurf, Claude Code, ChatGPT, local models) - [x] [qtype](https://github.com/VernonOY/qtype) integration for static code checks - [ ] Portfolio construction (factor → tradeable portfolio) - [ ] Market regime detection & factor-regime mapping - [ ] Factor crowding detection - [ ] Web UI dashboard ## License Apache 2.0 ## Contributing [See CONTRIBUTING.md](CONTRIBUTING.md) — add skills, data adapters, or improve methodology. ---

Stop writing boilerplate. Start finding alpha.

Built by quants who got tired of copy-pasting the same IC calculation for the 500th time.