HonestDiD

================

The HonestDiD R package implements the tools for robust inference and

sensitivity analysis for differences-in-differences and event study

designs developed in [Rambachan and Roth

(2022)](https://asheshrambachan.github.io/assets/files/hpt-draft.pdf).

There is also an [HonestDiD Stata

package](https://github.com/mcaceresb/stata-honestdid#honestdid), and a

[Shiny app](https://ccfang2.shinyapps.io/HonestDiDSenAnlys/) developed

by Chengcheng Fang.

## Background

The robust inference approach in Rambachan and Roth formalizes the

intuition that pre-trends are informative about violations of parallel

trends. They provide a few different ways of formalizing what this

means.

**Bounds on relative magnitudes.** One way of formalizing this idea is

to say that the violations of parallel trends in the post-treatment

period cannot be much bigger than those in the pre-treatment period.

This can be formalized by imposing that the post-treatment violation of

parallel trends is no more than some constant

larger than the maximum violation of parallel trends in the

pre-treatment period. The value of

= 1, for instance, imposes that the post-treatment violation of parallel

trends is no longer than the worst pre-treatment violation of parallel

trends (between consecutive periods). Likewise, setting

= 2 implies that the post-treatment violation of parallel trends is no

more than twice that in the pre-treatment period.

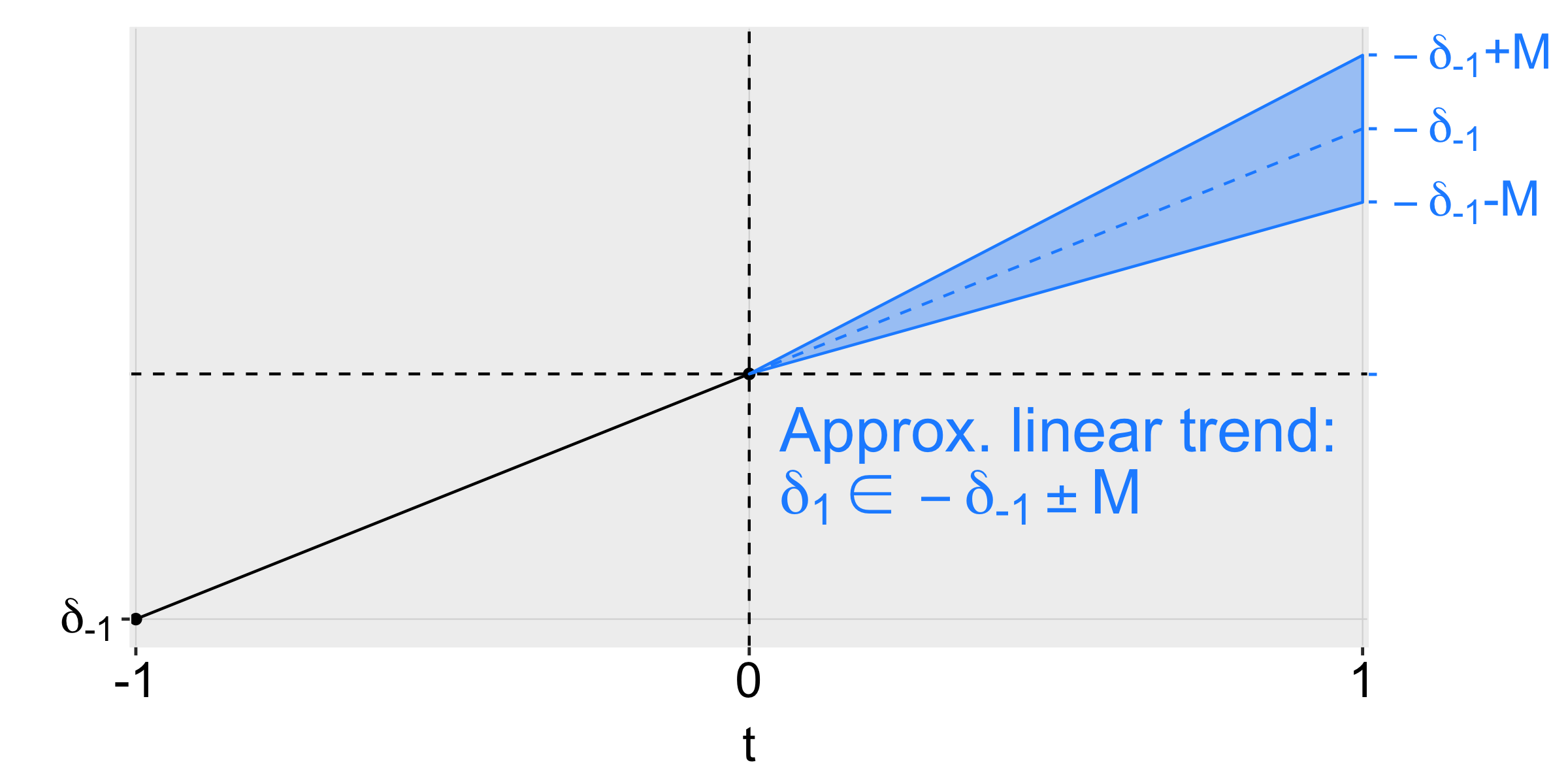

**Smoothness restrictions.** A second way of formalizing this is to say

that the post-treatment violations of parallel trends cannot deviate too

much from a linear extrapolation of the pre-trend. In particular, we can

impose that the slope of the pre-trend can change by no more than *M*

across consecutive periods, as shown in the figure below for an example

with three periods.

diagram-smoothness-restriction

Thus, imposing a smoothness restriction with *M* = 0 implies that the

counterfactual difference in trends is exactly linear, whereas larger

values of *M* allow for more non-linearity.

**Other restrictions**. The Rambachan and Roth framework allows for a

variety of other restrictions on the differences in trends as well. For

example, the smoothness restrictions and relative magnitudes ideas can

be combined to impose that the non-linearity in the post-treatment

period is no more than

times larger than that in the pre-treatment periods. The researcher can

also impose monotonicity or sign restrictions on the differences in

trends as well.

**Robust confidence intervals**. Given restrictions of the type

described above, Rambachan and Roth provide methods for creating robust

confidence intervals that are guaranteed to include the true parameter

at least 95% of the time when the imposed restrictions on satisfied.

These confidence intervals account for the fact that there is estimation

error both in the treatment effects estimates and our estimates of the

pre-trends.

**Sensitivity analysis**. The approach described above naturally lends

itself to sensitivity analysis. That is, the researcher can report

confidence intervals under different assumptions about how bad the

post-treatment violation of parallel trends can be (e.g., different

values of

or *M*.) They can also report the “breakdown value” of

(or *M*) for a particular conclusion – e.g. the largest value of

for which the effect is still significant.

## Package installation

The package may be installed by using the function `install_github()`

from the `remotes` package:

``` r

## Installation

# Install remotes package if not installed

install.packages("remotes")

# Turn off warning-error-conversion, because the tiniest warning stops installation

Sys.setenv("R_REMOTES_NO_ERRORS_FROM_WARNINGS" = "true")

# install from github

remotes::install_github("asheshrambachan/HonestDiD")

```

## Example usage – Medicaid expansions

As an illustration of the package, we will examine the effects of

Medicaid expansions on insurance coverage using publicly-available data

derived from the ACS. We first load the data and packages relevant for

the analysis.

``` r

#Install here, dplyr, did, haven, ggplot2, fixest packages from CRAN if not yet installed

#install.packages(c("here", "dplyr", "did", "haven", "ggplot2", "fixest"))

library(here)

library(dplyr)

library(did)

library(haven)

library(ggplot2)

library(fixest)

library(HonestDiD)

df <- read_dta("https://raw.githubusercontent.com/Mixtape-Sessions/Advanced-DID/main/Exercises/Data/ehec_data.dta")

head(df,5)

```

## # A tibble: 5 × 5

## stfips year dins yexp2 W

##

## 1 1 [alabama] 2008 [2008] 0.681 NA 613156

## 2 1 [alabama] 2009 [2009] 0.658 NA 613156

## 3 1 [alabama] 2010 [2010] 0.631 NA 613156

## 4 1 [alabama] 2011 [2011] 0.656 NA 613156

## 5 1 [alabama] 2012 [2012] 0.671 NA 613156

The data is a state-level panel with information on health insurance

coverage and Medicaid expansion. The variable `dins` shows the share of

low-income childless adults with health insurance in the state. The

variable `yexp2` gives the year that a state expanded Medicaid coverage

under the Affordable Care Act, and is missing if the state never

expanded.

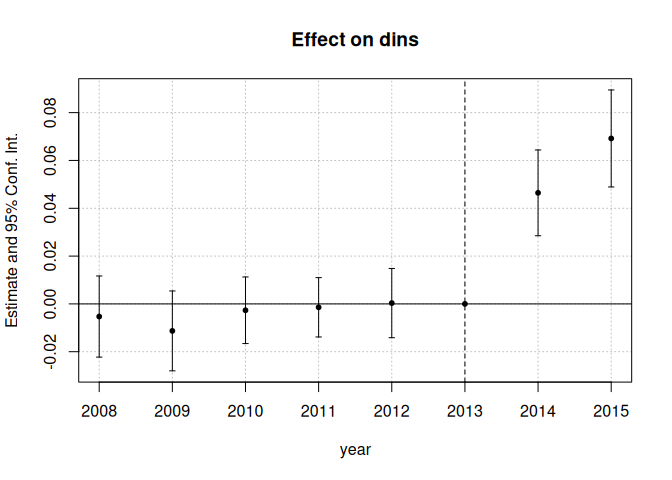

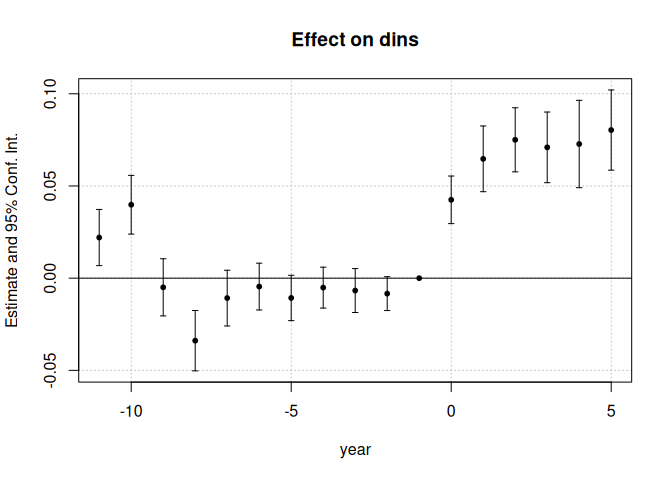

### Estimate the baseline DiD

For simplicity, we will first focus on assessing sensitivity to

violations of parallel trends in a non-staggered DiD (see below

regarding methods for staggered timing). We therefore restrict the

sample to the years 2015 and earlier, and drop the small number of

states who are first treated in 2015. We are now left with a panel

dataset where some units are first treated in 2014 and the remaining

units are not treated during the sample period. We can then estimate the

effects of Medicaid expansion using a canonical two-way fixed effects

event-study specification,

where D is 1 if a unit is first treated in 2014 and 0 otherwise.

``` r

df <- read_dta("https://raw.githubusercontent.com/Mixtape-Sessions/Advanced-DID/main/Exercises/Data/ehec_data.dta")

#Keep years before 2016. Drop the 2016 cohort

df_nonstaggered <- df %>% filter(year < 2016 &

(is.na(yexp2)| yexp2 != 2015) )

#Create a treatment dummy

df_nonstaggered <- df_nonstaggered %>% mutate(D = case_when( yexp2 == 2014 ~ 1,

T ~ 0))

#Run the TWFE spec

twfe_results <- fixest::feols(dins ~ i(year, D, ref = 2013) | stfips + year,

cluster = "stfips",

data = df_nonstaggered)

betahat <- summary(twfe_results)$coefficients #save the coefficients

sigma <- summary(twfe_results)$cov.scaled #save the covariance matrix

fixest::iplot(twfe_results)

```

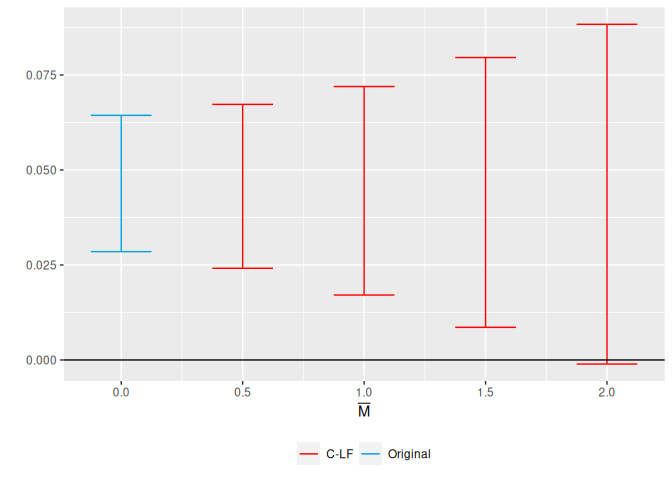

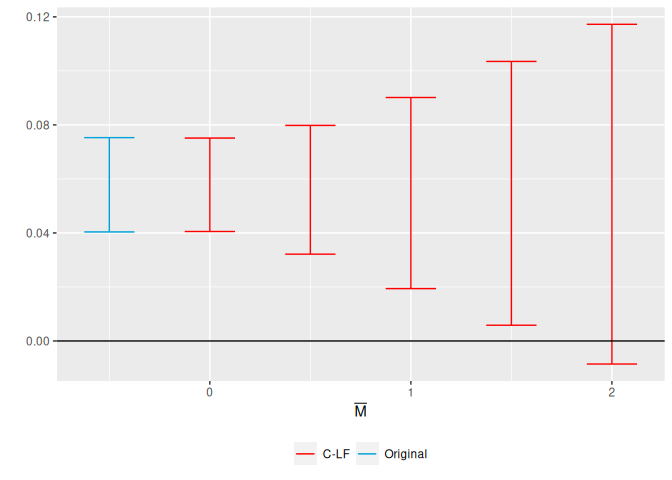

## Sensitivity analysis using relative magnitudes restrictions

We are now ready to apply the HonestDiD package to do sensitivity

analysis. Suppose we’re interested in assessing the sensitivity of the

estimate for 2014, the first year after treatment.

``` r

delta_rm_results <-

HonestDiD::createSensitivityResults_relativeMagnitudes(

betahat = betahat, #coefficients

sigma = sigma, #covariance matrix

numPrePeriods = 5, #num. of pre-treatment coefs

numPostPeriods = 2, #num. of post-treatment coefs

Mbarvec = seq(0.5,2,by=0.5) #values of Mbar

)

delta_rm_results

```

## # A tibble: 4 × 5

## lb ub method Delta Mbar

##

## 1 0.0241 0.0673 C-LF DeltaRM 0.5

## 2 0.0171 0.0720 C-LF DeltaRM 1

## 3 0.00859 0.0796 C-LF DeltaRM 1.5

## 4 -0.00107 0.0883 C-LF DeltaRM 2

The output of the previous command shows a robust confidence interval

for different values of

.

We see that the “breakdown value” for a significant effect is

= 2, meaning that the significant result is robust to allowing for

violations of parallel trends up to twice as big as the max violation in

the pre-treatment period.

We can also visualize the sensitivity analysis using the

`createSensitivityPlot_relativeMagnitudes`. To do this, we first have to

calculate the CI for the original OLS estimates using the

`constructOriginalCS` command. We then pass our sensitivity analysis and

the original results to the `createSensitivityPlot_relativeMagnitudes`

command.

``` r

originalResults <- HonestDiD::constructOriginalCS(betahat = betahat,

sigma = sigma,

numPrePeriods = 5,

numPostPeriods = 2)

HonestDiD::createSensitivityPlot_relativeMagnitudes(delta_rm_results, originalResults)

```

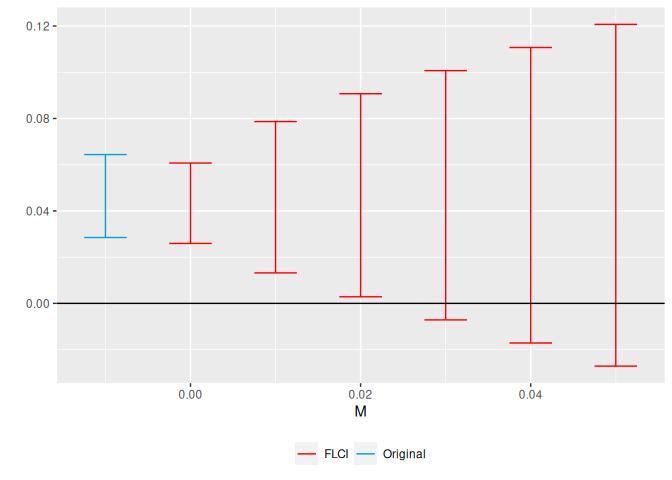

## Sensitivity Analysis Using Smoothness Restrictions

We can also do a sensitivity analysis based on smoothness restrictions –

i.e. imposing that the slope of the difference in trends changes by no

more than *M* between periods.

``` r

delta_sd_results <-

HonestDiD::createSensitivityResults(betahat = betahat,

sigma = sigma,

numPrePeriods = 5,

numPostPeriods = 2,

Mvec = seq(from = 0, to = 0.05, by =0.01))

delta_sd_results

```

## # A tibble: 6 × 5

## lb ub method Delta M

##

## 1 0.0259 0.0607 FLCI DeltaSD 0

## 2 0.0132 0.0787 FLCI DeltaSD 0.01

## 3 0.00286 0.0907 FLCI DeltaSD 0.02

## 4 -0.00714 0.101 FLCI DeltaSD 0.03

## 5 -0.0171 0.111 FLCI DeltaSD 0.04

## 6 -0.0271 0.121 FLCI DeltaSD 0.05

``` r

createSensitivityPlot(delta_sd_results, originalResults)

```

We see that the breakdown value for a significant effect is *M* ≈ 0.03,

meaning that we can reject a null effect unless we are willing to allow

for the linear extrapolation across consecutive periods to be off by

more than 0.03 percentage points.

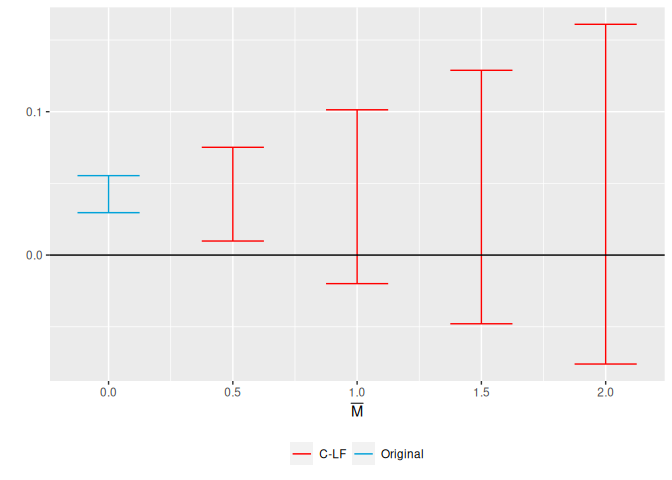

## Sensitivity Analysis for Average Effects or Other Periods

So far we have focused on the effect for the first post-treatment

period, which is the default in HonestDiD. If we are instead interested

in the average over the two post-treatment periods, we can use the

option `l_vec = c(0.5,0.5)`. More generally, the package accommodates

inference on any scalar parameter of the form

*θ* = *l**v**e**c*′*τ**p**o**s**t*, where

*τ**p**o**s**t* = (*τ*1,…,*τ**T̄*)′ is

the vector of dynamic treatment effects. Thus, for example, setting

`l_vec = basisVector(2,numPostPeriods)` allows us to do inference on the

effect for the second period after treatment.

``` r

delta_rm_results_avg <-

HonestDiD::createSensitivityResults_relativeMagnitudes(betahat = betahat,

sigma = sigma,

numPrePeriods = 5,

numPostPeriods = 2, Mbarvec = seq(0,2,by=0.5),

l_vec = c(0.5,0.5))

originalResults_avg <- HonestDiD::constructOriginalCS(betahat = betahat,

sigma = sigma,

numPrePeriods = 5,

numPostPeriods = 2,

l_vec = c(0.5,0.5))

HonestDiD::createSensitivityPlot_relativeMagnitudes(delta_rm_results_avg, originalResults_avg)

```

## Regressions with controls

The parameters `betahat` and `sigma` should be the coefficients and

variance-covariance matrix for the **event-study** plot only. Sometimes

we may have regression results that contain both the event-study

coefficients and coefficients on other auxilliary variables

(e.g. controls). In this case, we should subset `betahat` and `sigma` to

the relevant coefficients corresponding to the event-study. An example

is given below:

``` r

# CREATE A FAKE CONTROL FOR ILLUSTRATION

set.seed(0)

df_nonstaggered$control <- rnorm(NROW(df_nonstaggered), 0, 1)

#Run the TWFE spec with the control added

# (Note that TWFEs with controls may not yield ATT under het effects; see Abadie 2005)

twfe_results <- fixest::feols(dins ~ i(year, D, ref = 2013) + control | stfips + year,

cluster = "stfips",

data = df_nonstaggered)

betahat <- summary(twfe_results)$coefficients #save the coefficients

sigma <- summary(twfe_results)$cov.scaled #save the covariance matrix

#Subset the coefficients to exclude the control, which here is in position 8

betahat <- betahat[-8]

sigma <-sigma[-8,-8]

HonestDiD::createSensitivityResults(betahat = betahat,

sigma = sigma,

numPrePeriods = 5,

numPostPeriods = 2,

Mvec = seq(from = 0, to = 0.05, by =0.01))

```

## # A tibble: 6 × 5

## lb ub method Delta M

##

## 1 0.0264 0.0607 FLCI DeltaSD 0

## 2 0.0128 0.0788 FLCI DeltaSD 0.01

## 3 0.00186 0.0908 FLCI DeltaSD 0.02

## 4 -0.00814 0.101 FLCI DeltaSD 0.03

## 5 -0.0181 0.111 FLCI DeltaSD 0.04

## 6 -0.0281 0.121 FLCI DeltaSD 0.05

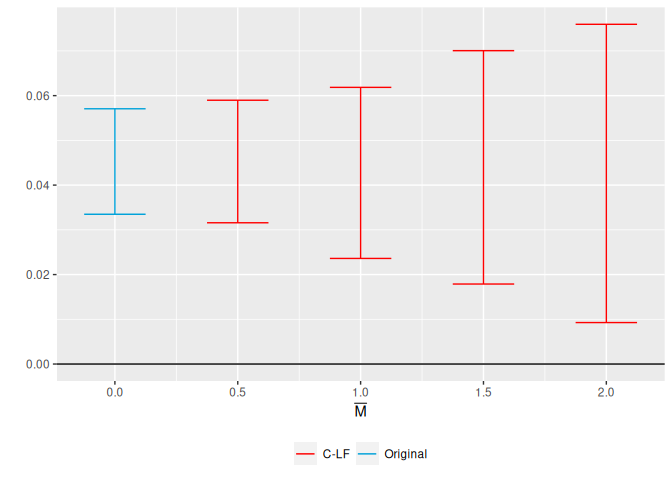

## Staggered timing

So far we have focused on a simple case without staggered timing.

Fortunately, the HonestDiD approach works well with recently-introduced

methods for DiD under staggered treatment timing. Below, we show how the

package can be used with the [fixest

package](https://lrberge.github.io/fixest/reference/sunab.html)

implementing Sun and Abraham or with the [did

package](https://github.com/bcallaway11/did#difference-in-differences-)

implementing Callaway and Sant’Anna. (See, also, the example on the did

package [website](https://github.com/pedrohcgs/CS_RR).) We are hoping to

more formally integrate the did and HonestDiD packages in the future –

stay tuned!

### Sun and Abraham

First, we import the function we created for extracting the

full-variance covariance matrix from `fixest` with `sunab`:

``` r

#' @description

#' This function takes a regression estimated using fixest with the sunab option

#' and extracts the aggregated event-study coefficients and their variance-covariance matrix

#' @param sunab_fixest The result of a fixest call using the sunab option

#' @returns A list containing beta (the event-study coefficients),

#' sigma (the variance-covariance matrix), and

#' cohorts (the relative times corresponding to beta, sigma)

sunab_beta_vcv <-

function(sunab_fixest){

## The following code block extracts the weights on individual coefs used in

# the fixest aggregation ##

sunab_agg <- sunab_fixest$model_matrix_info$sunab$agg_period

sunab_names <- base::names(sunab_fixest$coefficients)

sunab_sel <- base::grepl(sunab_agg, sunab_names, perl=TRUE)

sunab_names <- sunab_names[sunab_sel]

if(!base::is.null(sunab_fixest$weights)){

sunab_wgt <- base::colSums(sunab_fixest$weights * base::sign(stats::model.matrix(sunab_fixest)[, sunab_names, drop=FALSE]))

} else {

sunab_wgt <- base::colSums(base::sign(stats::model.matrix(sunab_fixest)[, sunab_names, drop=FALSE]))

}

#Construct matrix sunab_trans such that sunab_trans %*% non-aggregated coefs = aggregated coefs,

sunab_cohorts <- base::as.numeric(base::gsub(base::paste0(".*", sunab_agg, ".*"), "\\2", sunab_names, perl=TRUE))

sunab_mat <- stats::model.matrix(~ 0 + base::factor(sunab_cohorts))

sunab_trans <- base::solve(base::t(sunab_mat) %*% (sunab_wgt * sunab_mat)) %*% base::t(sunab_wgt * sunab_mat)

#Get the coefs and vcv

sunab_coefs <- sunab_trans %*% base::cbind(sunab_fixest$coefficients[sunab_sel])

sunab_vcov <- sunab_trans %*% sunab_fixest$cov.scaled[sunab_sel, sunab_sel] %*% base::t(sunab_trans)

base::return(base::list(beta = sunab_coefs,

sigma = sunab_vcov,

cohorts = base::sort(base::unique(sunab_cohorts))))

}

```

``` r

# Run fixest with sunab

df$year_treated <- ifelse(is.na(df$yexp2), Inf, df$yexp2)

formula_sunab <- dins ~ sunab(year_treated, year) | stfips + year

res_sunab <- fixest::feols(formula_sunab, cluster="stfips", data=df)

fixest::iplot(res_sunab)

```

``` r

# Extract the beta and vcv

beta_vcv <- sunab_beta_vcv(res_sunab)

# Run sensitivity analysis for relative magnitudes

kwargs <- list(betahat = beta_vcv$beta,

sigma = beta_vcv$sigma,

numPrePeriods = sum(beta_vcv$cohorts < 0),

numPostPeriods = sum(beta_vcv$cohorts > -1))

extra <- list(Mbarvec=seq(from = 0.5, to = 2, by = 0.5), gridPoints=100)

original_results <-

do.call(HonestDiD::constructOriginalCS, kwargs)

sensitivity_results <-

do.call(HonestDiD::createSensitivityResults_relativeMagnitudes,

c(kwargs, extra))

HonestDiD::createSensitivityPlot_relativeMagnitudes(sensitivity_results,

original_results)

```

### Callaway and Sant’Anna

First, we import the function Pedro Sant’Anna created for formatting did

output for HonestDiD:

``` r

#' @title honest_did

#'

#' @description a function to compute a sensitivity analysis

#' using the approach of Rambachan and Roth (2021)

#'

#' @param ... Parameters to pass to the relevant method.

honest_did <- function(...) UseMethod("honest_did")

#' @title honest_did.AGGTEobj

#'

#' @description a function to compute a sensitivity analysis

#' using the approach of Rambachan and Roth (2021) when

#' the event study is estimating using the `did` package

#'

#' @param es Result from aggte (object of class AGGTEobj).

#' @param e event time to compute the sensitivity analysis for.

#' The default value is `e=0` corresponding to the "on impact"

#' effect of participating in the treatment.

#' @param type Options are "smoothness" (which conducts a

#' sensitivity analysis allowing for violations of linear trends

#' in pre-treatment periods) or "relative_magnitude" (which

#' conducts a sensitivity analysis based on the relative magnitudes

#' of deviations from parallel trends in pre-treatment periods).

#' @param gridPoints Number of grid points used for the underlying test

#' inversion. Default equals 100. User may wish to change the number of grid

#' points for computational reasons.

#' @param ... Parameters to pass to `createSensitivityResults` or

#' `createSensitivityResults_relativeMagnitudes`.

honest_did.AGGTEobj <- function(es,

e = 0,

type = c("smoothness", "relative_magnitude"),

gridPoints = 100,

...) {

type <- match.arg(type)

# Make sure that user is passing in an event study

if (es$type != "dynamic") {

stop("need to pass in an event study")

}

# Check if used universal base period and warn otherwise

if (es$DIDparams$base_period != "universal") {

stop("Use a universal base period for honest_did")

}

# Recover influence function for event study estimates

es_inf_func <- es$inf.function$dynamic.inf.func.e

# Recover variance-covariance matrix

n <- nrow(es_inf_func)

V <- t(es_inf_func) %*% es_inf_func / n / n

# Check time vector is consecutive with referencePeriod = -1

referencePeriod <- -1

consecutivePre <- !all(diff(es$egt[es$egt <= referencePeriod]) == 1)

consecutivePost <- !all(diff(es$egt[es$egt >= referencePeriod]) == 1)

if ( consecutivePre | consecutivePost ) {

msg <- "honest_did expects a time vector with consecutive time periods;"

msg <- paste(msg, "please re-code your event study and interpret the results accordingly.", sep="\n")

stop(msg)

}

# Remove the coefficient normalized to zero

hasReference <- any(es$egt == referencePeriod)

if ( hasReference ) {

referencePeriodIndex <- which(es$egt == referencePeriod)

V <- V[-referencePeriodIndex,-referencePeriodIndex]

beta <- es$att.egt[-referencePeriodIndex]

} else {

beta <- es$att.egt

}

nperiods <- nrow(V)

npre <- sum(1*(es$egt < referencePeriod))

npost <- nperiods - npre

if ( !hasReference & (min(c(npost, npre)) <= 0) ) {

if ( npost <= 0 ) {

msg <- "not enough post-periods"

} else {

msg <- "not enough pre-periods"

}

msg <- paste0(msg, " (check your time vector; note honest_did takes -1 as the reference period)")

stop(msg)

}

baseVec1 <- basisVector(index=(e+1),size=npost)

orig_ci <- constructOriginalCS(betahat = beta,

sigma = V,

numPrePeriods = npre,

numPostPeriods = npost,

l_vec = baseVec1)

if (type=="relative_magnitude") {

robust_ci <- createSensitivityResults_relativeMagnitudes(betahat = beta,

sigma = V,

numPrePeriods = npre,

numPostPeriods = npost,

l_vec = baseVec1,

gridPoints = gridPoints,

...)

} else if (type == "smoothness") {

robust_ci <- createSensitivityResults(betahat = beta,

sigma = V,

numPrePeriods = npre,

numPostPeriods = npost,

l_vec = baseVec1,

...)

}

return(list(robust_ci=robust_ci, orig_ci=orig_ci, type=type))

}

```

``` r

###

# Run the CS event-study with 'universal' base-period option

## Note that universal base period normalizes the event-time minus 1 coef to 0

cs_results <- did::att_gt(yname = "dins",

tname = "year",

idname = "stfips",

gname = "yexp2",

data = df %>% mutate(yexp2 = ifelse(is.na(yexp2), 3000, yexp2)),

control_group = "notyettreated",

base_period = "universal")

es <- did::aggte(cs_results, type = "dynamic",

min_e = -5, max_e = 5)

#Run sensitivity analysis for relative magnitudes

sensitivity_results <-

honest_did(es,

e=0,

type="relative_magnitude",

Mbarvec=seq(from = 0.5, to = 2, by = 0.5))

HonestDiD::createSensitivityPlot_relativeMagnitudes(sensitivity_results$robust_ci,

sensitivity_results$orig_ci)

```

## Additional options and resources

See the previous package [vignette](https://github.com/asheshrambachan/HonestDiD/blob/fdadae33428a024df204c210da48cc5362966e89/vignettes/HonestDiD_Example.pdf) for additional examples and

package options, including incorporating sign and monotonicity

restrictions, and combining relative magnitudes and smoothness

restrictions.

You can also view a video presentation about this paper

[here](https://www.youtube.com/watch?v=6-NkiA2jN7U).

## Authors

- [Ashesh Rambachan](https://asheshrambachan.github.io/)

- [Jonathan Roth](https://www.jonathandroth.com/)

## Acknowledgements

This software package is based upon work supported by the National

Science Foundation Graduate Research Fellowship under Grant DGE1745303

(Rambachan) and Grant DGE1144152 (Roth). We thank [Mauricio Cáceres

Bravo](https://mcaceresb.github.io/) for his help in developing the

package.