![]()

![]() "

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "HedPhu1-uqXL"

},

"source": [

"# Log-Optimal Growth and the Kelly Criterion"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "Jc08h8eGuqXL"

},

"source": [

"This [IPython notebook](http://ipython.org/notebook.html) demonstrates the Kelly criterion and other phenomena associated with log-optimal growth."

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "LN9Xm4q0uqXM"

},

"source": [

"## Initializations"

]

},

{

"cell_type": "code",

"execution_count": null,

"metadata": {

"colab": {},

"colab_type": "code",

"id": "udCWC5J-uqXN"

},

"outputs": [],

"source": [

"%matplotlib notebook\n",

"\n",

"import matplotlib.pyplot as plt\n",

"import numpy as np\n",

"import random"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "ui0RvOnxuqXQ"

},

"source": [

"## What are the Issues in Managing for Optimal Growth?"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "Y0tFvIxuuqXQ"

},

"source": [

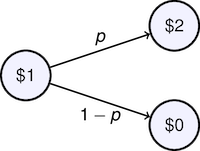

"Consider a continuing 'investment opportunity' for which, at each stage, an invested dollar will yield either two dollars with probability $p$ or nothing with probability $1-p$. You can think of this as a gambling game if you like, or as sequence of business investment decisions.\n",

"\n",

"\n",

"\n",

"Let $W_k$ be the wealth after $k$ stages in this sequence of decisions. At each stage $k$ there will be an associated return $R_k$ so that\n",

"\n",

"$$W_k = R_k W_{k-1}$$\n",

"\n",

"Starting with a wealth $W_0$, after $k$ stages our wealth will be\n",

"\n",

"$$W_k = R_kR_{k-1}\\cdots R_2R_1W_0$$\n",

"\n",

"Now let's consider a specific investment strategy. To avoid risking total loss of wealth in a single stage, we'll consider a strategy where we invest a fraction $\\alpha$ of our remaining wealth, and retain a fraction $1-\\alpha$ for future use. Under this strategy, the return $R_k$ is given by\n",

"\n",

"$$R_k = \\begin{cases} 1+\\alpha & \\mbox{with probability}\\quad p \\\\ 1-\\alpha & \\mbox{with probability}\\quad 1-p\\end{cases}$$\n",

"\n",

"How should we pick $\\alpha$? A small value means that wealth will grow slowly. A large value will risk more of our wealth in each trial."

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "d4wl2IfsuqXR"

},

"source": [

"## Why Maximizing Expected Wealth is a Bad Idea"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "e7ioaVPZuqXS"

},

"source": [

"At first glance, maximizing expected wealth seems like a reasonable investment objective. Suppose after $k$ stages we have witnessed $u$ profitable outcomes (i.e., 'wins'), and $k-u$ outcomes showing a loss. The remaining wealth will be given by\n",

"\n",

"$$W_k/W_0 = (1+\\alpha)^u(1-\\alpha)^{k-u}$$\n",

"\n",

"The binomial distribution gives the probability of observing $u$ 'wins' in $k$ trials\n",

"\n",

"$$Pr(u \\mbox{ wins in } k \\mbox{ trials}) = {k\\choose{u}}p^u (1-p)^{k-u}$$\n",

"\n",

"So the expected value of $W_k$ is given by\n",

"\n",

"$$E[W_k/W_0] = \\sum_{u=0}^{k} {k\\choose{u}}p^u (1-p)^{k-u}(1+\\alpha)^u(1-\\alpha)^{k-u}$$\n",

"\n",

"Next we plot $E[W_k/W_0]$ as a function of $\\alpha$. If you run this notebook on your own server, you can adjust $p$ and $K$ to see the impact of changing parameters."

]

},

{

"cell_type": "code",

"execution_count": null,

"metadata": {

"colab": {},

"colab_type": "code",

"id": "BUbFBBUfuqXT",

"outputId": "6128296e-5fc4-4e68-b45f-64db1c9b3eaa"

},

"outputs": [

{

"data": {

"application/vnd.jupyter.widget-view+json": {

"model_id": "90f394624e7448e6a425e2f5a18ad4ee"

}

},

"metadata": {

"tags": []

},

"output_type": "display_data"

}

],

"source": [

"from scipy.misc import comb\n",

"from ipywidgets import interact\n",

"\n",

"def sim(K = 40,p = 0.55):\n",

" alpha = np.linspace(0,1,100)\n",

" W = [sum([comb(K,u)*((p*(1+a))**u)*(((1-p)*(1-a))**(K-u)) \\\n",

" for u in range(0,K+1)]) for a in alpha]\n",

" plt.figure()\n",

" plt.plot(alpha,W,'b')\n",

" plt.xlabel('alpha')\n",

" plt.ylabel('E[W({:d})/W(0)]'.format(K))\n",

" plt.title('Expected Wealth after {:d} trials'.format(K))\n",

"\n",

"interact(sim,K=(1,60),p=(0.4,0.6,0.01));"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "Po0g0gTIuqXY"

},

"source": [

"This simulation suggests that if each stage is, on average, a winning proposition with $p > 0.5$, then expected wealth after $K$ stages is maximized by setting $\\alpha = 1$. This is a very risky strategy. \n",

"\n",

"To show how risky, the following cell simulates the behavior of this process for as a function of $\\alpha$, $p$, and $K$. Try different values of $\\alpha$ in the range from 0 to 1 to see what happens."

]

},

{

"cell_type": "code",

"execution_count": null,

"metadata": {

"colab": {},

"colab_type": "code",

"id": "tlVMPSGmuqXZ",

"outputId": "91df71c7-75e6-4e01-9cec-dbdf9cec4abd"

},

"outputs": [

{

"data": {

"application/vnd.jupyter.widget-view+json": {

"model_id": "00de5525a9e84114a4d03dcd75f5468d"

}

},

"metadata": {

"tags": []

},

"output_type": "display_data"

},

{

"data": {

"text/plain": [

"

"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "HedPhu1-uqXL"

},

"source": [

"# Log-Optimal Growth and the Kelly Criterion"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "Jc08h8eGuqXL"

},

"source": [

"This [IPython notebook](http://ipython.org/notebook.html) demonstrates the Kelly criterion and other phenomena associated with log-optimal growth."

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "LN9Xm4q0uqXM"

},

"source": [

"## Initializations"

]

},

{

"cell_type": "code",

"execution_count": null,

"metadata": {

"colab": {},

"colab_type": "code",

"id": "udCWC5J-uqXN"

},

"outputs": [],

"source": [

"%matplotlib notebook\n",

"\n",

"import matplotlib.pyplot as plt\n",

"import numpy as np\n",

"import random"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "ui0RvOnxuqXQ"

},

"source": [

"## What are the Issues in Managing for Optimal Growth?"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "Y0tFvIxuuqXQ"

},

"source": [

"Consider a continuing 'investment opportunity' for which, at each stage, an invested dollar will yield either two dollars with probability $p$ or nothing with probability $1-p$. You can think of this as a gambling game if you like, or as sequence of business investment decisions.\n",

"\n",

"\n",

"\n",

"Let $W_k$ be the wealth after $k$ stages in this sequence of decisions. At each stage $k$ there will be an associated return $R_k$ so that\n",

"\n",

"$$W_k = R_k W_{k-1}$$\n",

"\n",

"Starting with a wealth $W_0$, after $k$ stages our wealth will be\n",

"\n",

"$$W_k = R_kR_{k-1}\\cdots R_2R_1W_0$$\n",

"\n",

"Now let's consider a specific investment strategy. To avoid risking total loss of wealth in a single stage, we'll consider a strategy where we invest a fraction $\\alpha$ of our remaining wealth, and retain a fraction $1-\\alpha$ for future use. Under this strategy, the return $R_k$ is given by\n",

"\n",

"$$R_k = \\begin{cases} 1+\\alpha & \\mbox{with probability}\\quad p \\\\ 1-\\alpha & \\mbox{with probability}\\quad 1-p\\end{cases}$$\n",

"\n",

"How should we pick $\\alpha$? A small value means that wealth will grow slowly. A large value will risk more of our wealth in each trial."

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "d4wl2IfsuqXR"

},

"source": [

"## Why Maximizing Expected Wealth is a Bad Idea"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "e7ioaVPZuqXS"

},

"source": [

"At first glance, maximizing expected wealth seems like a reasonable investment objective. Suppose after $k$ stages we have witnessed $u$ profitable outcomes (i.e., 'wins'), and $k-u$ outcomes showing a loss. The remaining wealth will be given by\n",

"\n",

"$$W_k/W_0 = (1+\\alpha)^u(1-\\alpha)^{k-u}$$\n",

"\n",

"The binomial distribution gives the probability of observing $u$ 'wins' in $k$ trials\n",

"\n",

"$$Pr(u \\mbox{ wins in } k \\mbox{ trials}) = {k\\choose{u}}p^u (1-p)^{k-u}$$\n",

"\n",

"So the expected value of $W_k$ is given by\n",

"\n",

"$$E[W_k/W_0] = \\sum_{u=0}^{k} {k\\choose{u}}p^u (1-p)^{k-u}(1+\\alpha)^u(1-\\alpha)^{k-u}$$\n",

"\n",

"Next we plot $E[W_k/W_0]$ as a function of $\\alpha$. If you run this notebook on your own server, you can adjust $p$ and $K$ to see the impact of changing parameters."

]

},

{

"cell_type": "code",

"execution_count": null,

"metadata": {

"colab": {},

"colab_type": "code",

"id": "BUbFBBUfuqXT",

"outputId": "6128296e-5fc4-4e68-b45f-64db1c9b3eaa"

},

"outputs": [

{

"data": {

"application/vnd.jupyter.widget-view+json": {

"model_id": "90f394624e7448e6a425e2f5a18ad4ee"

}

},

"metadata": {

"tags": []

},

"output_type": "display_data"

}

],

"source": [

"from scipy.misc import comb\n",

"from ipywidgets import interact\n",

"\n",

"def sim(K = 40,p = 0.55):\n",

" alpha = np.linspace(0,1,100)\n",

" W = [sum([comb(K,u)*((p*(1+a))**u)*(((1-p)*(1-a))**(K-u)) \\\n",

" for u in range(0,K+1)]) for a in alpha]\n",

" plt.figure()\n",

" plt.plot(alpha,W,'b')\n",

" plt.xlabel('alpha')\n",

" plt.ylabel('E[W({:d})/W(0)]'.format(K))\n",

" plt.title('Expected Wealth after {:d} trials'.format(K))\n",

"\n",

"interact(sim,K=(1,60),p=(0.4,0.6,0.01));"

]

},

{

"cell_type": "markdown",

"metadata": {

"colab_type": "text",

"id": "Po0g0gTIuqXY"

},

"source": [

"This simulation suggests that if each stage is, on average, a winning proposition with $p > 0.5$, then expected wealth after $K$ stages is maximized by setting $\\alpha = 1$. This is a very risky strategy. \n",

"\n",

"To show how risky, the following cell simulates the behavior of this process for as a function of $\\alpha$, $p$, and $K$. Try different values of $\\alpha$ in the range from 0 to 1 to see what happens."

]

},

{

"cell_type": "code",

"execution_count": null,

"metadata": {

"colab": {},

"colab_type": "code",

"id": "tlVMPSGmuqXZ",

"outputId": "91df71c7-75e6-4e01-9cec-dbdf9cec4abd"

},

"outputs": [

{

"data": {

"application/vnd.jupyter.widget-view+json": {

"model_id": "00de5525a9e84114a4d03dcd75f5468d"

}

},

"metadata": {

"tags": []

},

"output_type": "display_data"

},

{

"data": {

"text/plain": [

"![]()

![]() "

]

}

],

"metadata": {

"colab": {

"collapsed_sections": [],

"name": "07.08-Log-Optimal-Growth-and-the-Kelly-Criterion.ipynb",

"provenance": [],

"version": "0.3.2"

},

"kernelspec": {

"display_name": "Python 3",

"language": "python",

"name": "python3"

},

"language_info": {

"codemirror_mode": {

"name": "ipython",

"version": 3

},

"file_extension": ".py",

"mimetype": "text/x-python",

"name": "python",

"nbconvert_exporter": "python",

"pygments_lexer": "ipython3",

"version": "3.7.3"

}

},

"nbformat": 4,

"nbformat_minor": 2

}

"

]

}

],

"metadata": {

"colab": {

"collapsed_sections": [],

"name": "07.08-Log-Optimal-Growth-and-the-Kelly-Criterion.ipynb",

"provenance": [],

"version": "0.3.2"

},

"kernelspec": {

"display_name": "Python 3",

"language": "python",

"name": "python3"

},

"language_info": {

"codemirror_mode": {

"name": "ipython",

"version": 3

},

"file_extension": ".py",

"mimetype": "text/x-python",

"name": "python",

"nbconvert_exporter": "python",

"pygments_lexer": "ipython3",

"version": "3.7.3"

}

},

"nbformat": 4,

"nbformat_minor": 2

}