# mortgagemath

[](https://github.com/murraystokely/mortgagemath/actions/workflows/tests.yml)

[](https://raw.githubusercontent.com/murraystokely/mortgagemath/main/coverage.svg)

[](https://pypi.org/project/mortgagemath/)

[](https://opensource.org/licenses/MIT)

[](https://pepy.tech/projects/mortgagemath)

[](https://mortgagemath.readthedocs.io/)

**Cent-accurate mortgage amortization for Python.** Every payment,

interest charge, and balance is computed with `Decimal` arithmetic

and validated against 46 published worked examples from government

regulators, bank servicing guides, and academic textbooks across

six countries. Zero runtime dependencies.

⭐ If mortgagemath helps your work, please

star the project on GitHub.

## Why mortgagemath?

Most mortgage libraries get the monthly payment right but diverge

from real lender statements by 1–4 cents per row. That drift

compounds over the schedule, breaks reconciliation against actual

bank statements, and makes audit work painful. `mortgagemath` is

built around the rounding and accounting conventions that actual

lenders use:

- **Decimal arithmetic** end-to-end (no float drift)

- **Configurable rounding** — `ROUND_UP`, `ROUND_DOWN`,

`ROUND_HALF_UP`, `ROUND_HALF_EVEN`

- **Two balance-tracking modes** — `ROUND_EACH` (US lender

statements) and `CARRY_PRECISION` (Excel / CRE textbooks)

- **Both day-count conventions** — 30/360 and Actual/360

- **International compounding** — monthly (US), semi-annual

(Canadian *Interest Act* j₂), and effective-annual

- **Flexible payment frequency** — monthly, bi-weekly, weekly,

quarterly, semi-monthly, or annual

- **Adjustable-rate mortgages** with rate schedules, payment

caps, and negative amortization

- **Interest-only periods** with automatic recast

- **Flat per-period fees** for French *assurance emprunteur*

and similar insurance loadings

- **Currency unit precision** — `Decimal("0.01")` for cents

or `Decimal("1")` for yen/won

- **Exact zero ending balance** — the final row trues up so

the schedule lands at exactly zero

- **46 validated fixtures** from the US, Canada, France, Japan,

Italy, and South Korea

## Installation

```sh

pip install mortgagemath

```

Requires Python 3.11+. Zero runtime dependencies.

```sh

python -m mortgagemath # self-check against reference values

```

## Quick example

A standard 30-year fixed-rate mortgage from the command line:

```sh

mortgagemath summary --principal 300000 --rate 6.5 --term-months 360

```

Or generate the full payment-by-payment schedule:

```sh

mortgagemath schedule --principal 300000 --rate 6.5 --term-months 360

```

The same loan from Python:

```python

from mortgagemath import us_30_year_fixed, periodic_payment, amortization_schedule

loan = us_30_year_fixed("300000", "6.5")

print(periodic_payment(loan)) # Decimal("1896.21")

sched = amortization_schedule(loan)

print(sched[1].interest) # Decimal("1625.00") — payment #1

print(sched[1].principal) # Decimal("271.21")

print(sched[-1].balance) # Decimal("0.00") — exact zero

print(sched[-1].total_interest) # Decimal("382628.90") — lifetime interest

```

The schedule is a plain `list` — `sched[0]` is the initial balance

(no payment), `sched[1]` through `sched[360]` are the monthly

payments.

For a quick summary without iterating the schedule:

```python

from mortgagemath import us_30_year_fixed, loan_summary

s = loan_summary(us_30_year_fixed("300000", "6.5"))

print(s.periodic_payment) # Decimal("1896.21")

print(s.total_interest) # Decimal("382628.90")

print(s.total_paid) # Decimal("682628.90")

print(s.num_payments) # 360

```

Convenience constructors like `us_30_year_fixed`, `us_15_year_fixed`,

`canada_fixed_j2`, `canada_accelerated_biweekly`, and

`us_actual_360_commercial` handle common cases. The full

`LoanParams` dataclass is available when you need every parameter

explicitly:

```python

from decimal import Decimal

from mortgagemath import LoanParams, PaymentRounding, amortization_schedule

loan = LoanParams(

principal=Decimal("162000"),

annual_rate=Decimal("3.875"),

term_months=360,

payment_rounding=PaymentRounding.ROUND_HALF_UP,

interest_rounding=PaymentRounding.ROUND_HALF_UP,

)

sched = amortization_schedule(loan)

print(sched[1].payment) # Decimal("761.78")

```

For Canadian j₂ mortgages, ARMs with rate and payment caps,

commercial Actual/360 with balloon, interest-only periods,

fee-loaded French schedules, and Japanese yen-precision loans,

see the **[Worked examples](docs/vignettes/rendered/examples.pdf)**

vignette.

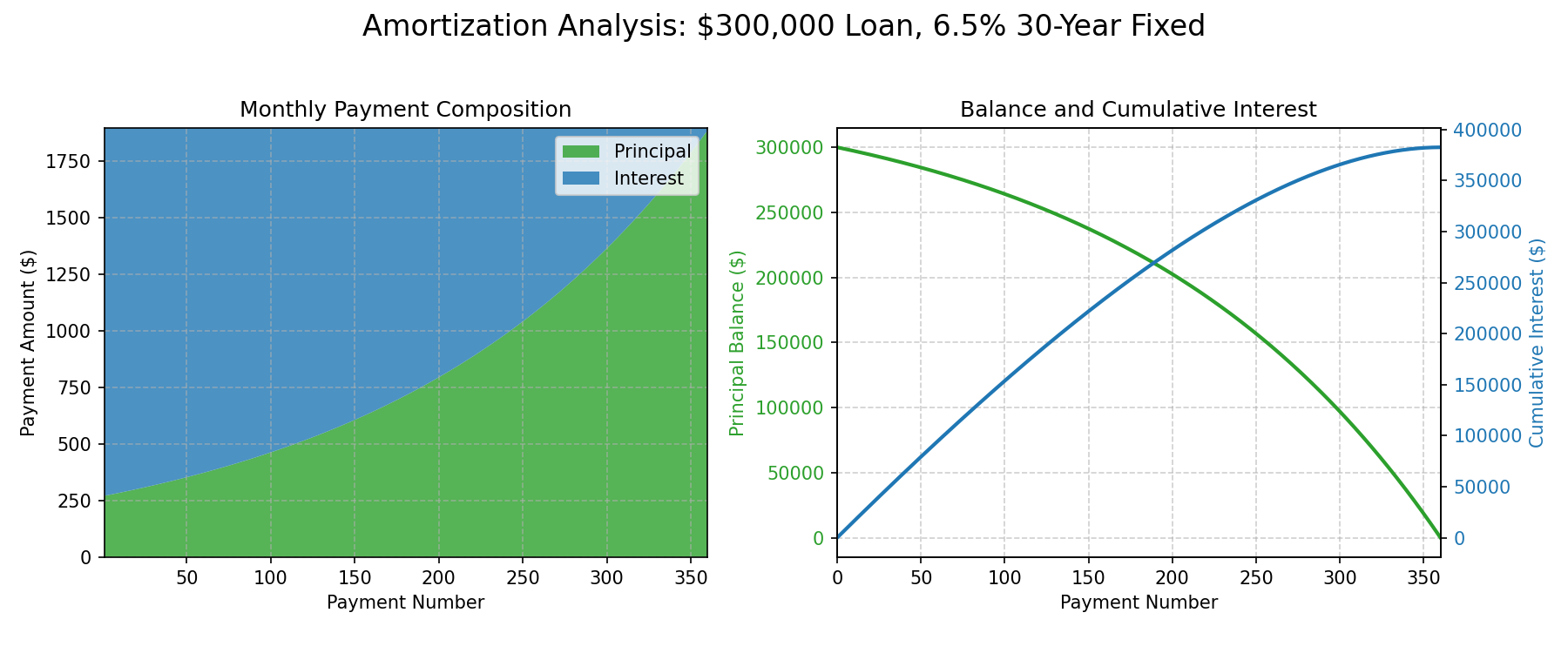

## Pandas and Matplotlib integration

`mortgagemath` returns pure Python dataclasses, so converting to a

`pandas.DataFrame` for analysis or plotting is one line:

```python

import pandas as pd

from mortgagemath import us_30_year_fixed, amortization_schedule

loan = us_30_year_fixed("300000", "6.5")

df = pd.DataFrame(amortization_schedule(loan))

```

See the **[Pandas and Data Visualization](docs/vignettes/rendered/pandas.pdf)** vignette for plotting examples and scenario analysis.

## What's validated

46 published amortization tables exercised by a test suite of more

than 400 tests that runs on every push and release. Every committed

fixture cell reproduces its source value to the cent (or yen). The

sources span six countries and a wide range of loan structures:

- **US regulatory** — CFPB sample disclosures, Reg Z Appendix H

ARM with 15 years of historical rate adjustments, FHLBB 1935

direct-reduction plan

- **US commercial** — Fannie Mae Multifamily Actual/360 with

balloon, Geltner CRE carry-precision

- **US textbooks** — OpenStax, Goldstein, Skinner (1913), Arcones

SOA Exam FM, Las Positas, Mississippi State Extension

- **Canada** — Olivier and eCampus Ontario semi-annual j₂

mortgages (monthly and quarterly), RBC accelerated bi-weekly

- **France** — MoneyVox *tableau d'amortissement* with *assurance

emprunteur* fee loading

- **Japan** — JHF Flat 35 and LoanKeisan full 360-row schedule

with yen-precision truncation rounding

- **Italy** — Solution Bank and BCC Brescia regulatory

transparency documents

- **South Korea** — Tistory worked mortgage with won-precision

- **Reference works** — TI BA II Plus official guidebook,

Wikipedia mortgage calculator

- **Synthetic** — half-cent rounding boundaries, zero-interest

edge case

See the **[Validation vignette](docs/vignettes/rendered/validation.pdf)**

for the full 46-fixture parameter matrix and bibliography.

## Documentation

| Resource | Audience |

|---|---|

| **[Read the Docs](https://mortgagemath.readthedocs.io/)** | Installation, quickstart, full API reference, changelog |

| **[At a glance](docs/vignettes/rendered/at-a-glance.pdf)** | 60-second orientation |

| **[Validation](docs/vignettes/rendered/validation.pdf)** | Audit / risk review — full fixture matrix + bibliography |

| **[Worked examples](docs/vignettes/rendered/examples.pdf)** | Picking the right configuration by country and loan type |

| **[History](docs/vignettes/rendered/history.pdf)** | Academic context — institutional and mathematical history of the level-payment mortgage |

| **[Pandas & Viz](docs/vignettes/rendered/pandas.pdf)** | DataFrames, plotting, and scenario analysis |

| **[HTML site](https://murraystokely.github.io/mortgagemath/)** | Vignettes with navigation and search |

## Reporting a discrepancy

Found a published example or a real lender statement that

`mortgagemath` doesn't reproduce to the cent? Two paths:

- **Reporters / users** — open an issue using the [Mortgage

example doesn't match](.github/ISSUE_TEMPLATE/mortgage-example.yml)

template. Paste the published values; no `pytest` needed.

- **Contributors** — add a paired TOML + CSV fixture under

`tests/schedules/`. See

[`tests/schedules/README.md`](tests/schedules/README.md) for

the schema and contribution workflow.

For unrelated bugs or feature requests, use the [Bug or feature

request](.github/ISSUE_TEMPLATE/bug-or-feature.yml) template.

## License

MIT