# rb3  [](https://www.repostatus.org/#active)

[](https://app.codecov.io/gh/wilsonfreitas/rb3?branch=main)

[](https://github.com/ropensci/rb3/actions)

[](https://CRAN.R-project.org/package=rb3)

[](https://cran.r-project.org/package=rb3)

[](https://github.com/ropensci/software-review/issues/534)

## Overview

[B3](https://www.b3.com.br) is the main financial exchange in Brazil,

offering access to trading systems for stocks, futures, options, and

other financial instruments. The `rb3` package provides tools for

downloading, processing, and analyzing market data from B3, including:

- **Stocks & Equities**: Historical price data through COTAHIST files

- **Futures Contracts**: Settlement prices for futures contracts

- **Yield Curves**: Historical yield curves calculated from futures

contracts

- **ETFs & BDRs**: Data for Exchange Traded Funds and Brazilian

Depositary Receipts

- **REITs (FIIs)**: Data for Brazilian Real Estate Investment Trusts

- **Options**: Equity and index options contracts

- **Market Indices**: B3 indices composition and historical data

The package uses webscraping tools to obtain data directly from [B3’s

website](https://www.b3.com.br), making it accessible in R as structured

datasets. These datasets are valuable for financial analysis, academic

research, and investment decision-making.

## Installation

``` r

# From CRAN (stable version)

install.packages("rb3")

# Development version from GitHub

if (!require(devtools)) install.packages("devtools")

devtools::install_github("ropensci/rb3")

```

## Basic Usage

### Downloading Data

Execute the following code to download all data you need to start

working with `rb3`:

``` r

# Set the rb3.cachedir folder - it must be executed before loading rb3 package

options(rb3.cachedir = "/path/to/your/custom/folder")

library(rb3)

library(bizdays)

# download COTAHIST data from 2000 to 2025

fetch_marketdata("b3-cotahist-yearly", year = 2000:2025)

# download futures settlement prices from 2000 to 2025

fetch_marketdata("b3-futures-settlement-prices", refdate = bizseq("2000-01-01", Sys.Date(), "Brazil/B3"))

# download yield curves from 2018 to 2025

fetch_marketdata("b3-reference-rates",

refdate = bizseq("2018-01-01", Sys.Date(), "Brazil/B3"),

curve_name = c("DIC", "DOC", "PRE")

)

# download indexes composition data - it is necessary to execute `indexes_get()`

fetch_marketdata("b3-indexes-composition")

# download current portfolio for all indexes

fetch_marketdata("b3-indexes-current-portfolio", index = indexes_get(), throttle = TRUE)

# download theoretical portfolio for all indexes

fetch_marketdata("b3-indexes-theoretical-portfolio", index = indexes_get(), throttle = TRUE)

# download historical data for all indexes

fetch_marketdata("b3-indexes-historical-data", index = indexes_get(), year = 2000:2025, throttle = TRUE)

```

### Market Data Templates

The `rb3` package uses a template system to standardize the downloading

and processing of different data types. To see available templates:

``` r

library(tidyverse)

library(bizdays)

library(rb3)

# List available templates

list_templates()

#> # A tibble: 9 × 2

#> Template Description

#>

#> 1 b3-bvbg-086 Arquivo de Preços de Mercado - BVBG-086

#> 2 b3-cotahist-daily Cotações Históricas do Pregão de Ações - Arq…

#> 3 b3-cotahist-yearly Cotações Históricas do Pregão de Ações - Arq…

#> 4 b3-futures-settlement-prices Preços de Ajustes Diários de Contratos Futur…

#> 5 b3-indexes-composition Composição dos índices da B3

#> 6 b3-indexes-current-portfolio Carteira teórica corrente dos índices da B3 …

#> 7 b3-indexes-historical-data Dados históricos e estatísticas dos índices …

#> 8 b3-indexes-theoretical-portfolio Carteira Teórica dos índices da B3 com pesos…

#> 9 b3-reference-rates Taxas referenciais

```

### Downloading Market Data

The main function for fetching data is `fetch_marketdata()`, which

downloads data based on a template and parameters:

``` r

# Download yield curve data for specific dates

fetch_marketdata("b3-reference-rates",

refdate = as.Date("2024-01-31"),

curve_name = "PRE"

)

# Download futures settlement prices

fetch_marketdata("b3-futures-settlement-prices",

refdate = as.Date("2024-01-31")

)

# Download yearly COTAHIST files

fetch_marketdata("b3-cotahist-yearly", year = 2023)

```

### Working with Historical Equity Data

``` r

# Access the data

ch <- cotahist_get("yearly")

# Filter for stocks

eq <- ch |>

filter(year(refdate) == 2023) |>

cotahist_filter_equity() |>

collect()

```

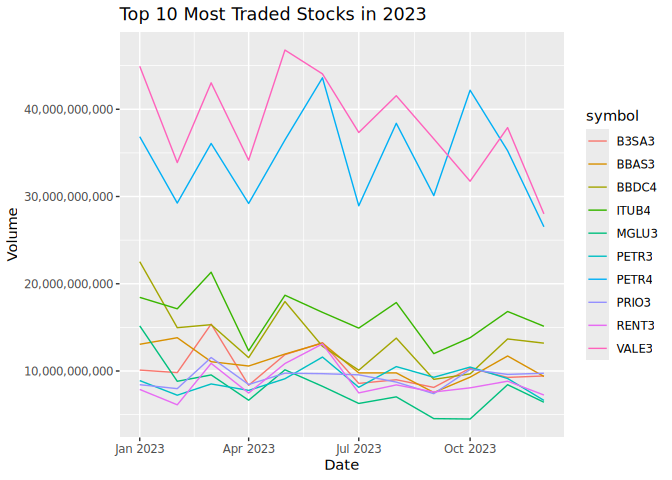

``` r

# Get top 10 most traded stocks

symbols <- eq |>

group_by(symbol) |>

summarise(volume = sum(volume)) |>

arrange(desc(volume)) |>

head(10) |>

pull(symbol)

# show top 10 most traded stocks

symbols

#> [1] "VALE3" "PETR4" "ITUB4" "BBDC4" "BBAS3" "B3SA3" "PRIO3" "PETR3" "RENT3"

#> [10] "MGLU3"

```

``` r

# Plot the most traded stocks grouped by month

eq |>

filter(symbol %in% symbols) |>

mutate(refdate = floor_date(refdate, "month")) |>

group_by(refdate, symbol) |>

summarise(volume = sum(volume)) |>

# Plot

ggplot(aes(x = refdate, y = volume, color = symbol)) +

geom_line() +

labs(

title = "Top 10 Most Traded Stocks in 2023",

x = "Date",

y = "Volume"

) +

scale_y_continuous(labels = scales::comma)

#> `summarise()` has grouped output by 'refdate'. You can override using the

#> `.groups` argument.

```

[](https://www.repostatus.org/#active)

[](https://app.codecov.io/gh/wilsonfreitas/rb3?branch=main)

[](https://github.com/ropensci/rb3/actions)

[](https://CRAN.R-project.org/package=rb3)

[](https://cran.r-project.org/package=rb3)

[](https://github.com/ropensci/software-review/issues/534)

## Overview

[B3](https://www.b3.com.br) is the main financial exchange in Brazil,

offering access to trading systems for stocks, futures, options, and

other financial instruments. The `rb3` package provides tools for

downloading, processing, and analyzing market data from B3, including:

- **Stocks & Equities**: Historical price data through COTAHIST files

- **Futures Contracts**: Settlement prices for futures contracts

- **Yield Curves**: Historical yield curves calculated from futures

contracts

- **ETFs & BDRs**: Data for Exchange Traded Funds and Brazilian

Depositary Receipts

- **REITs (FIIs)**: Data for Brazilian Real Estate Investment Trusts

- **Options**: Equity and index options contracts

- **Market Indices**: B3 indices composition and historical data

The package uses webscraping tools to obtain data directly from [B3’s

website](https://www.b3.com.br), making it accessible in R as structured

datasets. These datasets are valuable for financial analysis, academic

research, and investment decision-making.

## Installation

``` r

# From CRAN (stable version)

install.packages("rb3")

# Development version from GitHub

if (!require(devtools)) install.packages("devtools")

devtools::install_github("ropensci/rb3")

```

## Basic Usage

### Downloading Data

Execute the following code to download all data you need to start

working with `rb3`:

``` r

# Set the rb3.cachedir folder - it must be executed before loading rb3 package

options(rb3.cachedir = "/path/to/your/custom/folder")

library(rb3)

library(bizdays)

# download COTAHIST data from 2000 to 2025

fetch_marketdata("b3-cotahist-yearly", year = 2000:2025)

# download futures settlement prices from 2000 to 2025

fetch_marketdata("b3-futures-settlement-prices", refdate = bizseq("2000-01-01", Sys.Date(), "Brazil/B3"))

# download yield curves from 2018 to 2025

fetch_marketdata("b3-reference-rates",

refdate = bizseq("2018-01-01", Sys.Date(), "Brazil/B3"),

curve_name = c("DIC", "DOC", "PRE")

)

# download indexes composition data - it is necessary to execute `indexes_get()`

fetch_marketdata("b3-indexes-composition")

# download current portfolio for all indexes

fetch_marketdata("b3-indexes-current-portfolio", index = indexes_get(), throttle = TRUE)

# download theoretical portfolio for all indexes

fetch_marketdata("b3-indexes-theoretical-portfolio", index = indexes_get(), throttle = TRUE)

# download historical data for all indexes

fetch_marketdata("b3-indexes-historical-data", index = indexes_get(), year = 2000:2025, throttle = TRUE)

```

### Market Data Templates

The `rb3` package uses a template system to standardize the downloading

and processing of different data types. To see available templates:

``` r

library(tidyverse)

library(bizdays)

library(rb3)

# List available templates

list_templates()

#> # A tibble: 9 × 2

#> Template Description

#>

#> 1 b3-bvbg-086 Arquivo de Preços de Mercado - BVBG-086

#> 2 b3-cotahist-daily Cotações Históricas do Pregão de Ações - Arq…

#> 3 b3-cotahist-yearly Cotações Históricas do Pregão de Ações - Arq…

#> 4 b3-futures-settlement-prices Preços de Ajustes Diários de Contratos Futur…

#> 5 b3-indexes-composition Composição dos índices da B3

#> 6 b3-indexes-current-portfolio Carteira teórica corrente dos índices da B3 …

#> 7 b3-indexes-historical-data Dados históricos e estatísticas dos índices …

#> 8 b3-indexes-theoretical-portfolio Carteira Teórica dos índices da B3 com pesos…

#> 9 b3-reference-rates Taxas referenciais

```

### Downloading Market Data

The main function for fetching data is `fetch_marketdata()`, which

downloads data based on a template and parameters:

``` r

# Download yield curve data for specific dates

fetch_marketdata("b3-reference-rates",

refdate = as.Date("2024-01-31"),

curve_name = "PRE"

)

# Download futures settlement prices

fetch_marketdata("b3-futures-settlement-prices",

refdate = as.Date("2024-01-31")

)

# Download yearly COTAHIST files

fetch_marketdata("b3-cotahist-yearly", year = 2023)

```

### Working with Historical Equity Data

``` r

# Access the data

ch <- cotahist_get("yearly")

# Filter for stocks

eq <- ch |>

filter(year(refdate) == 2023) |>

cotahist_filter_equity() |>

collect()

```

``` r

# Get top 10 most traded stocks

symbols <- eq |>

group_by(symbol) |>

summarise(volume = sum(volume)) |>

arrange(desc(volume)) |>

head(10) |>

pull(symbol)

# show top 10 most traded stocks

symbols

#> [1] "VALE3" "PETR4" "ITUB4" "BBDC4" "BBAS3" "B3SA3" "PRIO3" "PETR3" "RENT3"

#> [10] "MGLU3"

```

``` r

# Plot the most traded stocks grouped by month

eq |>

filter(symbol %in% symbols) |>

mutate(refdate = floor_date(refdate, "month")) |>

group_by(refdate, symbol) |>

summarise(volume = sum(volume)) |>

# Plot

ggplot(aes(x = refdate, y = volume, color = symbol)) +

geom_line() +

labs(

title = "Top 10 Most Traded Stocks in 2023",

x = "Date",

y = "Volume"

) +

scale_y_continuous(labels = scales::comma)

#> `summarise()` has grouped output by 'refdate'. You can override using the

#> `.groups` argument.

```

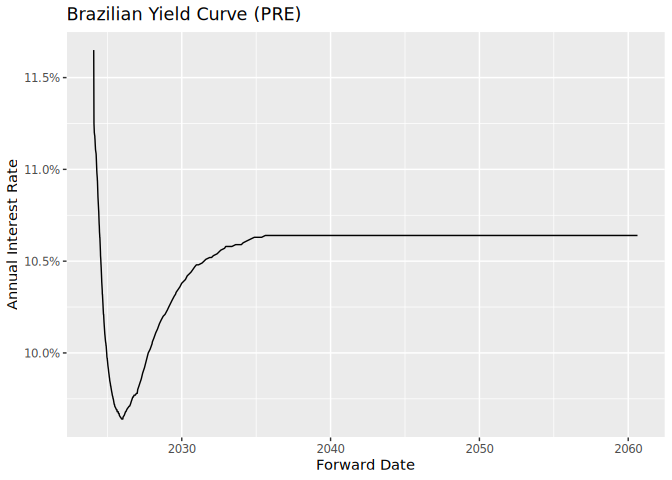

### Yield Curve Analysis

``` r

# Get Brazilian nominal yield curve (PRE)

yc_data <- yc_brl_get() |>

filter(refdate == "2024-01-31") |>

collect()

```

``` r

# Plot the yield curve

ggplot(yc_data, aes(x = forward_date, y = r_252)) +

geom_line() +

labs(

title = "Brazilian Yield Curve (PRE)",

x = "Forward Date",

y = "Annual Interest Rate"

) +

scale_y_continuous(labels = scales::percent)

```

### Yield Curve Analysis

``` r

# Get Brazilian nominal yield curve (PRE)

yc_data <- yc_brl_get() |>

filter(refdate == "2024-01-31") |>

collect()

```

``` r

# Plot the yield curve

ggplot(yc_data, aes(x = forward_date, y = r_252)) +

geom_line() +

labs(

title = "Brazilian Yield Curve (PRE)",

x = "Forward Date",

y = "Annual Interest Rate"

) +

scale_y_continuous(labels = scales::percent)

```

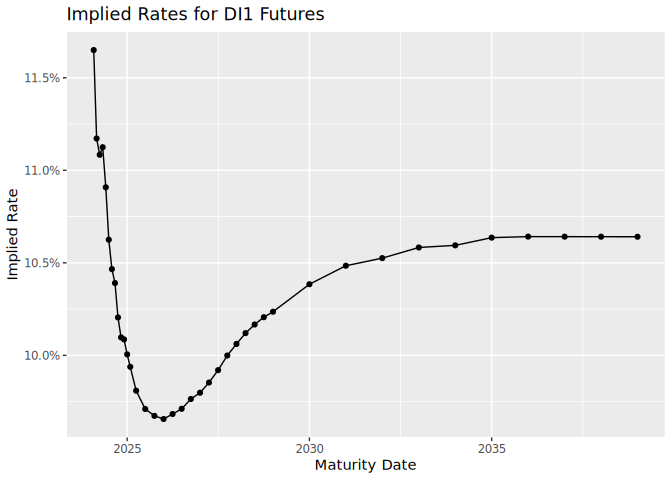

### Futures Contracts

``` r

# Get futures settlement prices

futures_data <- futures_get() |>

filter(commodity == "DI1") |>

collect()

```

``` r

# Calculate implied rates

di1_futures <- futures_data |>

mutate(

maturity_date = maturitycode2date(maturity_code),

business_days = bizdays(refdate, maturity_date, "Brazil/ANBIMA"),

implied_rate = (100000 / price)^(252 / business_days) - 1

)

# Plot the implied rates

ggplot(di1_futures, aes(x = maturity_date, y = implied_rate)) +

geom_line() +

geom_point() +

labs(

title = "Implied Rates for DI1 Futures",

x = "Maturity Date",

y = "Implied Rate"

) +

scale_y_continuous(labels = scales::percent)

```

### Futures Contracts

``` r

# Get futures settlement prices

futures_data <- futures_get() |>

filter(commodity == "DI1") |>

collect()

```

``` r

# Calculate implied rates

di1_futures <- futures_data |>

mutate(

maturity_date = maturitycode2date(maturity_code),

business_days = bizdays(refdate, maturity_date, "Brazil/ANBIMA"),

implied_rate = (100000 / price)^(252 / business_days) - 1

)

# Plot the implied rates

ggplot(di1_futures, aes(x = maturity_date, y = implied_rate)) +

geom_line() +

geom_point() +

labs(

title = "Implied Rates for DI1 Futures",

x = "Maturity Date",

y = "Implied Rate"

) +

scale_y_continuous(labels = scales::percent)

```

## Documentation

For comprehensive documentation and examples, visit:

- [Package Website](https://ropensci.github.io/rb3/)

- Vignettes (in-depth tutorials):

- [Getting

Started](https://ropensci.github.io/rb3/articles/Getting-started.html)

- [Fetching Historical Equity

Data](https://ropensci.github.io/rb3/articles/Fetching-historical-equity-data.html)

- [Analyzing B3 Index

Data](https://ropensci.github.io/rb3/articles/Fetching-historical-index-data.html)

- [How to Compute Historical Rates from B3 Future

Prices](https://ropensci.github.io/rb3/articles/Fetching-historical-future-rates.html)

- [Fetching B3 Yield

Curves](https://ropensci.github.io/rb3/articles/Fetching-historical-yield-curve.html)

## Citation

If you use `rb3` in your research, please cite it:

To cite rb3 in publications use:

Download and parse public files released by B3 and convert them into

useful formats and data structures common to data analysis

practitioners.

A BibTeX entry for LaTeX users is

@Manual{rb3-package,

title = {Download and Parse Public Data Released by B3 Exchange},

author = {Wilson Freitas and Marcelo Perlin},

year = {2023},

note = {R package version 0.0.8},

url = {https://github.com/ropensci/rb3},

}

## Documentation

For comprehensive documentation and examples, visit:

- [Package Website](https://ropensci.github.io/rb3/)

- Vignettes (in-depth tutorials):

- [Getting

Started](https://ropensci.github.io/rb3/articles/Getting-started.html)

- [Fetching Historical Equity

Data](https://ropensci.github.io/rb3/articles/Fetching-historical-equity-data.html)

- [Analyzing B3 Index

Data](https://ropensci.github.io/rb3/articles/Fetching-historical-index-data.html)

- [How to Compute Historical Rates from B3 Future

Prices](https://ropensci.github.io/rb3/articles/Fetching-historical-future-rates.html)

- [Fetching B3 Yield

Curves](https://ropensci.github.io/rb3/articles/Fetching-historical-yield-curve.html)

## Citation

If you use `rb3` in your research, please cite it:

To cite rb3 in publications use:

Download and parse public files released by B3 and convert them into

useful formats and data structures common to data analysis

practitioners.

A BibTeX entry for LaTeX users is

@Manual{rb3-package,

title = {Download and Parse Public Data Released by B3 Exchange},

author = {Wilson Freitas and Marcelo Perlin},

year = {2023},

note = {R package version 0.0.8},

url = {https://github.com/ropensci/rb3},

}