# FinSTaR: Towards Financial Reasoning with Time Series Reasoning Models

**FinSTaR** (**Fin**ancial Time **S**eries **T**hinking **a**nd **R**easoning) is the first Time Series Reasoning Model (TSRM) designed specifically for the financial domain. It employs two structurally different chain-of-thought (CoT) strategies tailored to the properties of financial reasoning:

- (1) **Compute-in-CoT** for *assessment* tasks (deterministic, computable from observable prices)

- (2) **Scenario-Aware CoT** for *prediction* tasks (probabilistic, subject to unobservable factors)

---

## Overview

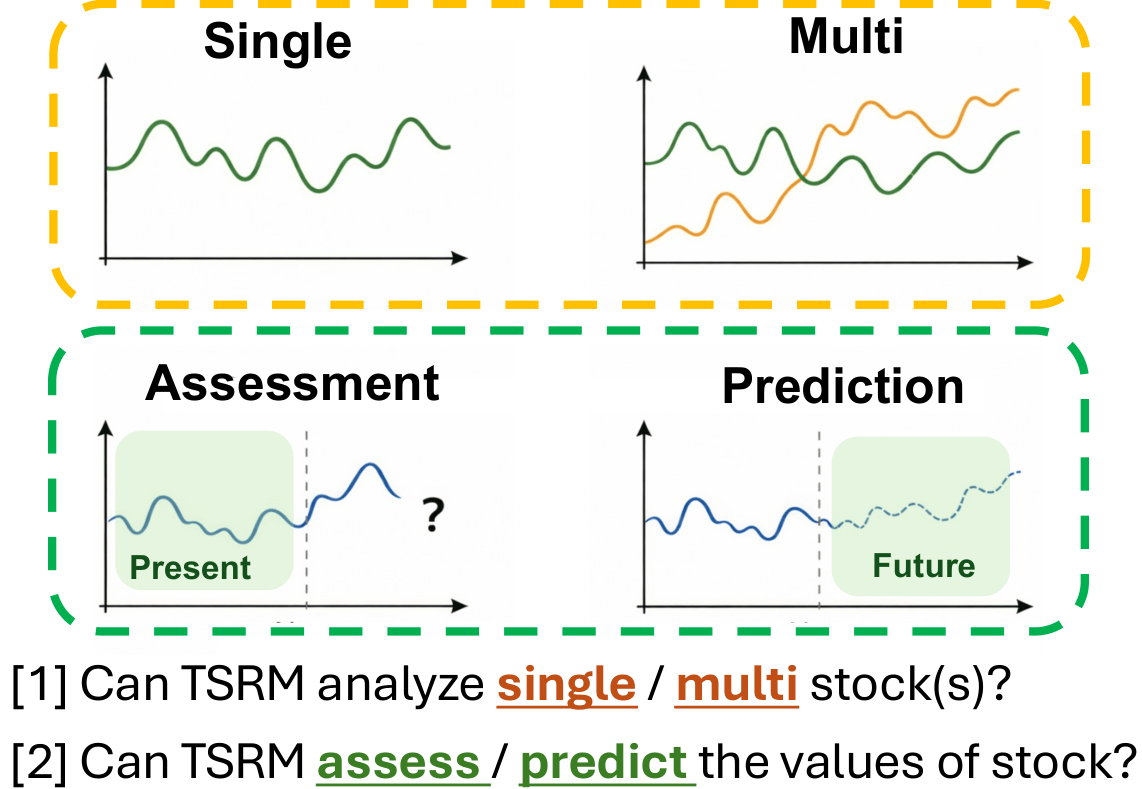

### Four Capability Categories

We define core capabilities of a Financial TSRM along two axes, forming a 2x2 taxonomy:

| | **Single-Stock** | **Multi-Stock** |

|---|---|---|

| **Assessment** | Drawdown, Volatility Regime, Trend Direction | Correlation |

| **Prediction** | Event Response, Support/Resistance, Drawdown Recovery, Volatility Forecast | Relative Performance, Pair Convergence |

### Key Results

| Model | Assessment Avg. | Prediction Avg. | Overall |

|---|---|---|---|

| Qwen2.5-7B (zero-shot) | 53.5 | 50.3 | 51.6 |

| TimeOmni-1-7B (zero-shot) | 48.3 | 53.2 | 51.3 |

| Qwen2.5-7B (SFT w/ CoT) | 67.7 | 51.1 | 57.8 |

| **FinSTaR (Ours)** | **95.0** | **68.2** | **78.9** |

---

## Installation

```bash

git clone https://github.com/seunghan96/FinSTaR.git

cd FinSTaR

pip install -r requirements.txt

```

---

## FinTSR-Bench

### Data Generation

FinTSR-Bench is constructed from 250 S&P 500 stocks (2010-2025). To generate the benchmark from raw stock data:

```bash

# Step 1: Generate QA pairs (10 tasks, ~3,500 samples each)

python src/data_generation/generate_qa_10tasks.py \

--data_dir raw_stock_data/ \

--output_dir data/raw/ \

--samples_per_task 3500

# Step 2: Generate CoT annotations and prepare final data

python src/data_generation/prepare_final_data.py \

--input_dir data/raw/ \

--output_dir data/

```

### Data Structure

```

data/

├── train_cot.json # 35K samples with CoT annotations

├── train_ao.json # 35K samples (answer-only)

├── test_sft.json # Test A: ID stocks, OOD period (10K)

├── test_b_ood_stock.json # Test B: OOD stocks, ID period (10K)

└── test_c_ood_stock_period.json # Test C: OOD stocks + period (10K)

```

### Data Format

Each sample follows the chat format:

```json

{

"task": "F1_drawdown",

"answer": "C",

"conversations": [

{"role": "user", "content": "You are analyzing the stock AAPL. Below are the daily closing prices (120 days): [...]"},

{"role": "assistant", "content": "\nStep 1 — Find the peak price: ...\n\n(C)"}

],

"metadata": {"peak": 182.63, "current": 161.42, "drawdown": 0.116}

}

```

---

## Training

### Quick Start

```bash

# Train FinSTaR (TimeOmni-1-7B backbone, LoRA, 4 epochs)

accelerate launch --num_processes 2 --mixed_precision bf16 \

src/training/train.py \

--model_dir anton-hugging/TimeOmni-1-7B \

--train_file data/train_cot.json \

--output_dir checkpoints/finstar \

--lora_r 32 --lora_alpha 64 \

--batch_size 1 --grad_accum 16 \

--max_length 4096 --num_epochs 4 --lr 5e-5

```

### Training Configurations

| Config | Backbone | CoT | Description |

|---|---|---|---|

| `02_cot_train_timeomni.sh` | TimeOmni-1-7B | Compute + Scenario | **FinSTaR** (main) |

| `03_cot_train_qwen.sh` | Qwen2.5-7B | Compute + Scenario | SFT baseline (w/ CoT) |

| `04_ao_train_timeomni.sh` | TimeOmni-1-7B | None (answer-only) | Ablation (w/o CoT) |

| `05_ao_train_qwen.sh` | Qwen2.5-7B | None (answer-only) | SFT baseline (w/o CoT) |

---

## Evaluation

### Zero-Shot Evaluation

```bash

# Evaluate any model zero-shot on FinTSR-Bench

python src/evaluation/inference.py \

--model_dir anton-hugging/TimeOmni-1-7B \

--test_file data/test_sft.json \

--output_dir results/timeomni_zs_test_a

```

### FinSTaR Evaluation

```bash

# Evaluate FinSTaR (LoRA adapter)

python src/evaluation/inference.py \

--model_dir anton-hugging/TimeOmni-1-7B \

--lora_dir checkpoints/finstar/lora \

--test_file data/test_sft.json \

--output_dir results/finstar_test_a

```

### Forecasting Baselines

```bash

# Statistical baselines (Last Value, MA, ETS, Drift, Momentum)

bash scripts/12_statistical_baselines.sh

# Deep learning baselines (PatchTST, DLinear, Chronos, etc.)

bash scripts/13_dl_baselines.sh

```

---

## Project Structure

```

FinSTaR/

├── README.md

├── requirements.txt

├── configs/

│ └── accelerate_config.yaml # Multi-GPU training config

├── src/

│ ├── data_generation/ # FinTSR-Bench construction

│ │ ├── generate_qa_10tasks.py # QA pair generation (10 tasks)

│ │ ├── generate_cot.py # Compute-in-CoT annotation

│ │ ├── generate_compute_cot.py # Extended CoT with computation

│ │ ├── prepare_final_data.py # Final data preparation

│ │ ├── prepare_fair_data.py # Fair evaluation data

│ │ └── utils.py # Financial indicators & utilities

│ ├── training/

│ │ ├── train.py # LoRA SFT training

│ │ ├── data_utils.py # Dataset & prompt utilities

│ │ └── train_utils.py # Model loading & LoRA config

│ └── evaluation/

│ ├── inference.py # Batch inference (vLLM)

│ ├── get_score.py # Metric computation

│ └── utils.py # Evaluation helpers

├── scripts/ # Experiment shell scripts

│ ├── 01_zs.sh # Zero-shot baselines

│ ├── 02_cot_train_timeomni.sh # FinSTaR training

│ ├── 06_cot_eval_timeomni.sh # FinSTaR evaluation

│ └── ...

└── data/ # FinTSR-Bench (generate via src/data_generation/)

```

---

## Citation

If you find this work useful, please cite:

```bibtex

@article{lee2026finstar,

title={FinSTaR: Towards Financial Reasoning with Time Series Reasoning Models},

author={Lee, Seunghan and Seo, Jun and Lee, Jaehoon and Yoo, Sungdong and Kim, Minjae and Lim, Tae Yoon and Kang, Dongwan and Choi, Hwanil and Lee, Soonyoung and Ahn, Wonbin},

journal={arXiv preprint arXiv:2605.03460},

year={2026}

}

```

## Acknowledgements

FinSTaR builds upon [TimeOmni-1](https://arxiv.org/abs/2509.24803) as its backbone.

We thank the TimeOmni team for releasing model weights. Stock price data is sourced from publicly available S&P 500 historical data.

## Contact

Seunghan Lee — seunghan.lee@lgresearch.ai