#include <pricingengine.hpp>

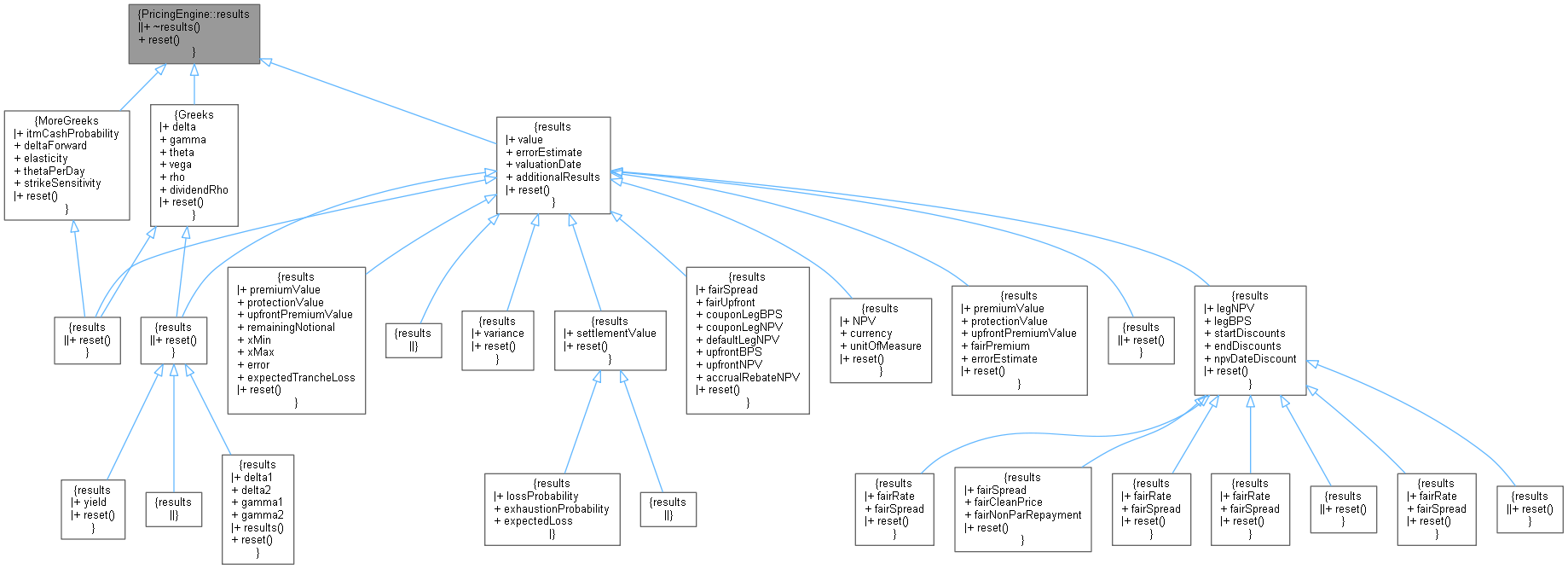

Inheritance diagram for PricingEngine::results:

Inheritance diagram for PricingEngine::results: Collaboration diagram for PricingEngine::results:

Collaboration diagram for PricingEngine::results:

Public Member Functions | |

| virtual | ~results ()=default |

| virtual void | reset ()=0 |

Detailed Description

Definition at line 51 of file pricingengine.hpp.

Constructor & Destructor Documentation

◆ ~results()

|

virtualdefault |

Member Function Documentation

◆ reset()

|

pure virtual |

Implemented in EnergyCommodity::results, NthToDefault::results, SyntheticCDO::results, EverestOption::results, PathMultiAssetOption::results, IrregularSwap::results, Instrument::results, AssetSwap::results, Bond::results, CPISwap::results, CreditDefaultSwap::results, FixedVsFloatingSwap::results, FloatFloatSwap::results, MargrabeOption::results, MultiAssetOption::results, NonstandardSwap::results, OneAssetOption::results, Swap::results, VarianceSwap::results, YearOnYearInflationSwap::results, Greeks, and MoreGreeks.