5.6 Using the t-Statistic in Regression when the Sample Size Is Small

The three OLS assumptions discussed in Chapter 4 (see Key Concept 4.3) are the foundation for the results on the large sample distribution of the OLS estimators in the simple regression model. What can be said about the distribution of the estimators and their \(t\)-statistics when the sample size is small and the population distribution of the data is unknown? Provided that the three least squares assumptions hold and the errors are normally distributed and homoskedastic (we refer to these conditions as the homoskedastic normal regression assumptions), we have normally distributed estimators and \(t\)-distributed test statistics in small samples.

Recall the definition of a \(t\)-distributed variable

\[ \frac{Z}{\sqrt{W/M}} \sim t_M,\]

where \(Z\) is a standard normal random variable, \(W\) is \(\chi^2\) distributed with \(M\) degrees of freedom and \(Z\) and \(W\) are independent. See section 5.6 in the book for a more detailed discussion of the small sample distribution of \(t\)-statistics in regression methods.

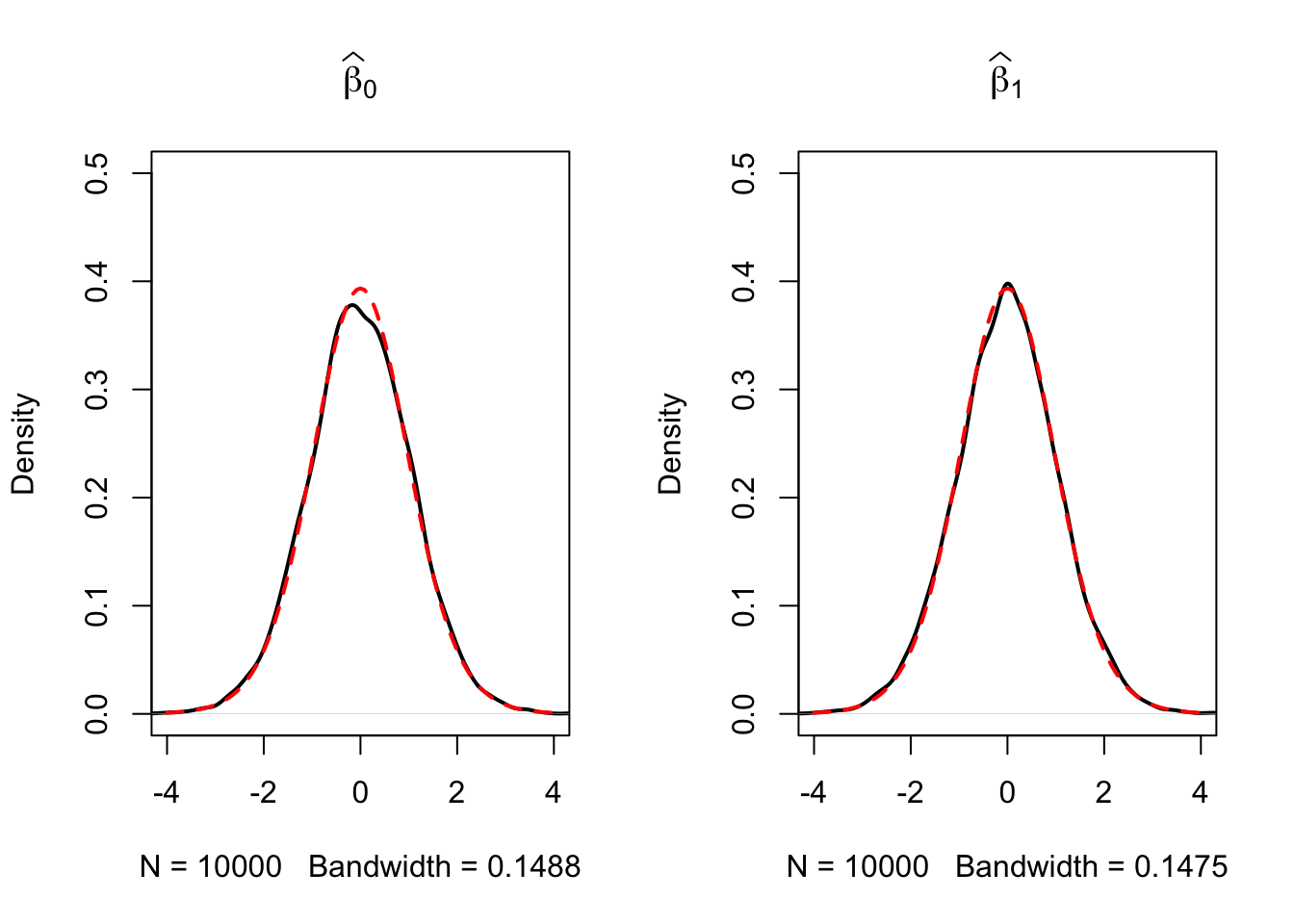

Let us simulate the distribution of regression \(t\)-statistics based on a large number of small random samples, say \(n=20\), and compare the simulated distributions to the theoretical distributions which should be \(t_{18}\), the \(t\)-distribution with \(18\) degrees of freedom (recall that \(\text{DF}=n-k-1\)).

# initialize two vectors

beta_0 <- c()

beta_1 <- c()

# loop sampling / estimation / t statistics

for (i in 1:10000) {

X <- runif(20, 0, 20)

Y <- rnorm(n = 20, mean = X)

reg <- summary(lm(Y ~ X))

beta_0[i] <- (reg$coefficients[1, 1] - 0)/(reg$coefficients[1, 2])

beta_1[i] <- (reg$coefficients[2, 1] - 1)/(reg$coefficients[2, 2])

}

# plot the distributions and compare with t_18 density:

# divide plotting area

par(mfrow = c(1, 2))

# plot the simulated density of beta_0

plot(density(beta_0),

lwd = 2 ,

main = expression(widehat(beta)[0]),

xlim = c(-4, 4),

ylim=c(0,0.5))

# add the t_18 density to the plot

curve(dt(x, df = 18),

add = T,

col = "red",

lwd = 2,

lty = 2)

# plot the simulated density of beta_1

plot(density(beta_1),

lwd = 2,

main = expression(widehat(beta)[1]),

xlim = c(-4, 4),

ylim=c(0,0.5))

# add the t_18 density to the plot

curve(dt(x, df = 18),

add = T,

col = "red",

lwd = 2,

lty = 2)

The outcomes are consistent with our expectations: the empirical distributions of both the estimators seem to track the theoretical \(t_{18}\) distribution quite closely.